Year-End Tax Tips

How to reduce your bill

We are getting near the end of the tax year (30 June), so you might want to consider ways to reduce your business’ tax bill.

The two simplest ways to do this are to reduce assessable income or increase deductible expenditure. Either way, the business’ taxable income (and thus the amount of tax payable) is reduced.

One way to reduce assessable income for the current income year is to delay sending an invoice to a customer until after 30 June, if your business reports income on a cash basis. Of course, cash flow issues may dictate otherwise.

If you are in the process of selling property and the profit will be taxable as a capital gain, you could defer the sale until the next income year – but remember that the liability to pay capital gains tax (CGT) arises when you exchange contracts and not on settlement.

You can increase deductible expenditure by bringing it forward from the next income year to the current income year. This is particularly useful where an immediate deduction is available — for example, for certain depreciating assets if you are a small business, start-up costs and certain prepaid expenses.

Charitable donations are a good way to increase your deductions. If you are not sure if a donation will be deductible, you can check the deductibility status of charities at https://www.abn.business.gov.au/Tools/DgrListing. In certain circumstances, a deduction is available where trading stock is donated. Don’t forget to ask for a receipt.

What are the benefits?

If you are a sole trader or a partner in a partnership, the benefits of reducing your taxable income could include:

- reducing your marginal tax rate, for example, from 37% to 30%, or from 30% to 16%; and

- avoiding liability for the Medicare levy surcharge (MLS) (at least 1% of your income for MLS purposes) if you do not have appropriate level of private health insurance hospital cover.

Tip!

As the end of the income year approaches, talk to your tax adviser about ways to minimise your tax bill.

Small business instant asset write-off

The instant asset write-off (IAWO) threshold for small businesses (aggregated turnover less than $10 million) is $20,000 for the current income year (2024–25). This means that a small business can fully deduct the cost of eligible depreciating assets that cost less than $20,000 (after claiming any GST credit to which the business is entitled) if they are first used or installed ready for use for a taxable purpose by 30 June 2025.

It is proposed that the IAWO threshold for 2025–26 will also be $20,000, but this measure is not yet law. If it becomes law, the IAWO threshold will revert to the standard amount of $1,000 from 1 July 2026. If it does not become law, the IAWO threshold for 2025–26 will be $1,000.

Division 7A issues

If you operate your business through a company, you will need to consider any arrangements between the company and associated entities, such as shareholders and trusts, involving a loan, the forgiveness of a debt or the use of the company’s assets, to see if a deemed dividend under Division 7A might arise.

You should ensure that the required minimum yearly repayments (MYR) under complying Division 7A loans made before 1 July 2024 are made by 30 June 2025. Appropriate directors’ resolutions are needed for any dividends declared by 30 June that will be ‘offset’ against a shareholder’s obligation to make the MYR.

The ATO is continuing to treat unpaid present entitlements (UPEs) of corporate beneficiaries as Division 7A loans, as it seeks special leave from the High Court to appeal a recent Full Federal Court decision (the Bendel case) that held a UPE was not a loan for the purposes of Division 7A.

Tip!

Division 7A can be a minefield. Talk to your tax adviser to avoid being assessed on an unfranked deemed dividend.

Bad debts

Your business may be entitled to a deduction for bad debts provided the debt is written off before the end of the income year. A debt that is merely doubtful is not deductible.

Writing off a bad debt does not necessarily require highly technical accounting entries. It is sufficient that some form of written record is kept to evidence the decision to write off the debt from the accounts. A directors’ resolution should be sufficient.

The debt must have been owed to you and is genuinely bad. This means it must be an amount that you have determined is unlikely to be recovered through any reasonable and commercial attempts.

Unless your business is a money-lending business, a bad debt deduction is not allowed if the debt has not been previously included in assessable income. So, if your business accounts for assessable income on a cash basis, an amount is not included in assessable income until it is received. Therefore, writing off a debt for an amount of unpaid income will have no income tax consequences for your business, as it has never been previously assessed.

If you operate your business through a company, the continuity of ownership or the same/similar business tests must be satisfied. Different tests apply if you operate your business through a trust, depending on the type of trust. Only one test applies — the income injection test — if the trust has made a family trust election (FTE).

Trustee resolutions

If you operate your business through a trust and you wish to make beneficiaries presently entitled to trust income for the 2024–25 income year, you should ensure your trustee resolutions are effective. This includes where you may want to make beneficiaries specifically entitled to franked dividends and capital gains that are included in trust income to stream these amounts.

Note that you do not have to prepare the trust accounts by 30 June to make beneficiaries presently entitled to trust income.

It is important that the trustee:

- makes decisions consistent with the terms of the trust deed. Check that the trust has not vested, as this may impact distribution decisions;

- consider who the intended beneficiaries are and their entitlement to income and capital under the trust deed. If the trustee has made an FTE or interposed entity election (IEE), this may have a tax impact on distribution decisions;

- notify beneficiaries of their entitlements to allow beneficiaries to correctly report distributions in their tax returns, preventing trust income from being omitted;

- follows any requirements in the trust deed governing the making of trustee resolutions, including the need to make the resolution in writing and when it is required to be made (there is no standard ATO format). Resolutions making one or more beneficiaries presently entitled to the trust income need to be made by the end of the income year;

- ensures that resolutions are unambiguous; and

- if the trust has capital gains or franked distributions the trustee would like to stream to beneficiaries, confirm the trust deed does not prevent this and that the trustee has complied with the legislative requirements relating to streaming these amounts.

Trustee checklist

To help trustees, the ATO has published a useful checklist in the form of a series of questions.

- Do you have a complete copy of the trust deed?

- Who can you appoint income or capital to?

- Has the trust vested?

- Is there an FTE in force for the trust?

- When do you have to make resolutions?

- Does a resolution have to be in writing?

- Is the wording of your resolution clear and unambiguous?

- Is the entitlement vested?

- Can the entitlement be taken away?

- How should you calculate and report the income of the trust?

- Are you ‘streaming’ capital gains or franked distributions?

- Are you seeking to ‘stream’ other types of income?

- Have all entitled beneficiaries quoted their tax file number (TFN) to you?

Family trusts

Family trust distribution tax (FTDT) happens when a trust that has made an FTE, or an entity that has made an IEE, makes a distribution outside the ‘family group’ of the individual specified in the FTE. This includes when distributing to another entity. The rate of FTDT is 47%.

So, where an FTE or IEE has been made, it is important to identify who is in the family group.

For non-fixed (discretionary) trusts to be within the family group of the individual specified in the FTE of another trust, they would need to have either:

- an FTE with the same specified individual in place; or

- an IEE as a member of the specified individual’s family group.

There is also a risk of not satisfying the qualified person rules where dividends are paid to a discretionary trust that has not made a family trust election. This means there could be restrictions or even the inability for the trust to pass on to beneficiaries franking credits attached to distributions of dividend income.

Tip!

Talk to your tax adviser – they can help you ensure that trustee resolutions are effective and that no liability to FTDT will arise.

From the ATO

Take charge of your upcoming employer obligations

It is time to review your business’ upcoming employer and superannuation obligations.

It is important to keep on top of your obligations as an employer. As the end of the financial year approaches, check what you need to do and take note of upcoming key dates.

Superannuation guarantee

- All superannuation guarantee (SG) contributions for the June 2025 quarter must be paid by 28 July 2025, in full, on time and to the right fund. For the quarter ending 30 June 2025, the 11.5% SG rate should be applied to salary and wage payments made before 1 July 2025.

- The SG rate Increases to 12% on 1 July 2025. This rate applies to payments of salary and wages to employees and certain contractors on and after 1 July 2025, even if some or all of the pay period it relates to is before 1 July 2025.

PAYG withholding

- From 1 July 2025, some pay as you go (PAYG) withholding schedules and tax tables will be updated. Use the correct tax tables to work out how much to withhold from your employees’ payments. Update your payroll software to withhold, report and pay the correct amount of tax.

Single touch payroll reporting

- A Single Touch Payroll (STP) finalisation declaration must be completed by 14 July 2025. This must cover all employees for whom you have paid and reported through STP so they have the right information to lodge their income tax returns.

- Finalise all employees whom you have paid in the financial year, even those you have not paid for a while, like terminated employees.

- If you change payroll software providers, finalise your records before you change. This ensures you and your employees have accurate information during tax time.

Other matters

Routinely review your payroll policies and procedures for any changes that impact your business, and put good record keeping practices in place.

Stay on top of your reporting, lodgment and payment deadlines to avoid penalties.

Get your deferral request right the first time

A lodgment deferral gives you extra time to lodge a document without incurring a failure to lodge on time (FTL) penalty. A lodgment deferral can help your business if it is experiencing exceptional or unforeseen circumstances which impact its ability to lodge on time.

The ATO is seeing an increasing number of lodgment deferral requests that fail to provide enough information or provide only generic information that does not support the reason for the request.

Information that must be provided to support a deferral request includes:

- what the exceptional or unforeseen circumstances are that your business is experiencing;

- when the exceptional or unforeseen circumstances occurred, whether they are ongoing or when they were resolved;

- how those circumstances have affected your business’ ability to lodge by the due date;

- why the request is being submitted after the lodgment due date (if applicable).

If sufficient information is not provided, the ATO will be unable to assess the request and it may be declined. Other reasons why a request may be declined are:

- your business has a record of late lodgments, including poor compliance with deferred due dates; and

- the ATO has started lodgment compliance action against your business.

Matters the ATO considers

Matters that the ATO considers when deciding whether it is fair and reasonable to grant your business a deferral include:

- the reason your business is unable to lodge on time;

- the size and structure of your business (large corporate entities are more likely to have the ability and resources to overcome circumstances that might affect their ability to not lodge by the due date);

- the risk to revenue;

- your business’ compliance history as a whole (that is, lodgment of taxation returns, activity statements and other documents, payments on time and previous dealings with the ATO);

- the length of time needed to lodge the document (a deferral will usually be granted if your business has a good compliance history and requests a short period of additional time to lodge); and

- any other relevant information that includes the individual circumstances.

Exceptional or unforeseen circumstances

The ATO generally considers it fair and reasonable to grant a deferral where the inability to lodge by the due date is reasonably attributed to exceptional or unforeseen circumstances.

- Exceptional or unforeseen circumstances may include:

- natural disasters or other disasters or events that may have, or have had, a significant impact on individuals, regions or particular industries;

- impeded access to records (for example, records seized during a police search or retained as evidence in a court matter);

- the serious illness or death of a family member, tax professional or critical staff member;

- considerable lack of knowledge and understanding of taxation obligations; and

- system issues, either with ATO online services or the entity’s business system.

PAYG instalments for business and investment income

Pay as you go (PAYG) instalments are regular prepayments of tax on your business and investment income. By paying regular instalments throughout the year, you should not have a large tax bill when you lodge your tax return.

PAYG instalments are reassessed after you lodge your tax return. If you have higher or lower business and investment income in your latest tax return, your instalment amount or rate may change.

If you think you will earn business and investment income over the threshold, it is a good idea to voluntarily choose to pay PAYG instalments.

If you pay PAYG instalments using the amount method, your instalments have increased by the gross domestic product (GDP) adjustment factor. For the 2024–25 income year, the GDP adjustment factor is 6%.

The ATO encourages you to review your tax position regularly and vary your PAYG instalments if needed, to reflect your expected tax for the year and to avoid penalties.

Tip!

Talk to your tax adviser if you think you may need to vary your or your business’ PAYG instalments.

Don’t get caught out by GST

GST registration and payment is an ongoing area of concern for the ATO. The ATO estimates that the community is missing out on almost $8 billion in GST each year that has not been collected due to non-compliance. Small businesses failing to comply with GST obligations contribute significantly to this gap.

Not every small business needs to be registered for GST, but when their GST turnover is $75,000 or more, or they provide taxi, limousine or ride-sourcing services, they must register and collect GST and then pay this to the ATO.

Small businesses who do not understand their GST obligations can often be caught out when it comes time to pay.

Tip!

Do not be tempted to dip into amounts set aside to pay GST, PAYG withholding or SG for your employees to manage your cash flow. Talk to your professional adviser if you are having cash flow problems.

Small business focus areas

Most small businesses try to do the right thing. But the ATO will take firmer action on those who knowingly do the wrong thing, to prevent them from gaining an unfair advantage over others.

The risks the ATO is currently focused on are:

- Business income is not personal income — where business owners use business money and assets for personal benefit;

- Deductions and concessions — non-commercial business losses, small business CGT concessions and small business boost measures;

- Operating outside of the system — GST registration and income of taxi, limousine and ride-sourcing services and contractors omitting income;

- Building good habits — entities moving from quarterly to monthly GST reporting and getting ready for business.

Tip!

If anything in the list above rings an alarm bell, talk to your tax adviser.

Changes to car thresholds from 1 July

Income tax

The car limit for 2025–-26 is $69,674 (the same as for 2024–25).

This is the highest value you can use to calculate depreciation on a car, where you:

- use the car for business purposes; and

- first use or lease the car in the 2025–26 income year.

As a business owner, you can claim a tax deduction on expenses for motor vehicles you use for business purposes.

If you are using a motor vehicle for both business and private purposes, you can claim a deduction only for the business part. You must be able to show the percentage you claim as business use and have records to support your claim.

Goods and services tax

If you are buying a car and the price is more than the car limit, the most GST credit you can claim (except in certain circumstances) is one-eleventh of the car limit. For 2025–26, the most GST credit you can claim is therefore $6,334 (that is, 1/11 × $69,674).

You need to claim GST credits within the 4-year time limit.

You cannot claim a credit for luxury car tax (LCT) when you buy a luxury car. This is even if you use it for business purposes.

Luxury car tax

The LCT threshold for 2025–26 is:

- $91,387 for fuel-efficient vehicles; and

- $80,567 for all other luxury vehicles.

From 1 July 2025, the definition of a fuel-efficient vehicle is changing. The change reduces the maximum fuel consumption for a car to be considered fuel-efficient from 7 litres per 100 kilometres to 3.5 litres per 100 kilometres. The indexation rates applying to the thresholds for fuel-efficient vehicles and other vehicles will be aligned.

If you are a dealer buying luxury cars under quote, you need to properly quote to meet your obligations.

EV home charging costs

The ATO is proposing to update its guidelines (PCG 2024/2) on electric vehicle (EV) home charging costs. The updated guidelines will provide guidance and a method for calculating electricity costs, for FBT and income tax purposes, when charging a plug-in hybrid electric vehicle (PHEV) at home. Currently, the guidelines apply only to EVs.

The new methodology will allow you to work out the total fuel expenses for a PHEV (by adding the actual petrol costs to the total electricity cost). This will apply to:

- an employer which provides PHEVs to staff for personal use;

- individuals (sole traders and employees) who incur work-related car expenses when they charge their PHEV at their home.

The ATO welcomes feedback on its proposed update by 24 July 2025.

FBT and car parking

Your business will provide a car parking fringe benefit to an employee if, on any day, all the following occur:

- your employee parks their car (or a car your business provides them) in a place that you own, lease or control (your business premises) which is at or near their primary place of employment;

- the business premises are within 1 kilometre (by the shortest practicable route) of a commercial parking station that charges an all-day parking fee greater than the car parking threshold ($11.03 for the 2025–26 FBT year) on both the first day of the FBT year (1 April 2025 for the 2025–26 FBT year) and the day the benefit is provided;

- the car is parked for more than 4 hours between 7.00 am and 7.00 pm;

- the employee drives their car between home and work, or vice versa, at least once;

- your business is not exempt from car parking fringe benefits.

Exemptions from car parking fringe benefits

Your business will not have to pay FBT for providing an employee with car parking, if any of the following apply:

- the employee has a disability – the employee must both be legally entitled to use a parking bay marked with the international symbol of access and have a valid accessibility parking permit displayed on the car;

- your business is a small business and the parking is not provided in a commercial car park – a small business for these purposes is one with gross total income less than $10 million and aggregated turnover is less than $50 million. This exemption does not apply if the business is a listed public company or a subsidiary of a listed public company;

- your business is an exempt employer – this category includes registered charities, non-profit scientific institutions, public educational institutions, public or not-for-profit hospitals and public ambulance services (in the case of hospitals and ambulance services, the benefit must be within the employee capping threshold).

If you provide car parking occasionally, it may qualify for the minor benefits exemption if it has a value of less than $300 and it would be considered unreasonable to treat it as a fringe benefit.

Note that car parking benefits provided to an associate of an employee may also be subject to FBT.

Tip!

If your business provides car parking benefits to employees (or any other benefits), talk to your tax adviser to see if your business will be liable to pay FBT.

Selling a business

The sale of a business generally occurs through the disposal of either:

- the shares or other ownership interests in the entity that conducts the business; or

- all the tangible and intangible assets in the business.

When preparing to dispose of your business, you should consider your tax governance for the transaction and the tax consequences.

Both the vendor and purchaser need to retain documentation evidencing the transactions, including:

- contracts;

- minutes of meetings recording why the business is being sold and decisions relating to the transaction by the directors and other key decision makers;

- communications between the vendor and purchaser relating to the negotiations, including any allowance for liabilities;

- details of the assets disposed of under the contract, the apportionment of the purchase price to the various assets and the basis for the apportionment;

- CGT calculations, including the allocation of the purchase price to depreciating assets, the basis for this allocation;

- any advice detailing why the particular tax position has been taken;

- settlement documentation;

- asset registers; and

- trustee resolutions creating income or capital entitlements in favour of beneficiaries.

Revenue or capital transaction

Where you dispose of an asset, you need to determine whether it should be treated as a revenue or capital transaction.

Disposing of a business to a related party

Where you dispose of the business to a related party, you should get an independent valuation of the business, including the goodwill, assets and contractual rights being disposed of. (See also ‘Transferring your business to family members’ below.)

Interest expense

There may be an impact on the interest expense that can be deducted under the thin capitalisation rules if the disposal of an ownership interest in a business results in a change to the entity’s debt to equity ratio. You may need to recalculate this at the relevant time.

Note that the thin capitalisation rules do not apply to an entity for an income year if the total debt deductions of the entity and all its associate entities for that year are $2 million or less.

Disposing of part of a business

You may partially dispose of your business by:

- creating a new class of shareholders or unit holders, or by amending rights for existing share classes;

- disposing of a portion of shares;

- retiring from a partnership; or

- admitting a new partner into your partnership.

As a result of the above changes, you may need to amend key documents such as the company’s constitution, trust deed or partnership agreement.

The rights of the existing shareholders or unitholders may also be affected. Where this occurs, the existing shareholders, unitholders and partners should consider any tax consequences, such as capital gains, value shifting and limitations on future deductions or capital losses.

More complex business disposals

More complex or non-traditional business disposals often give rise to a range of tax issues and require risk mitigation. Good tax governance will ensure that you identify, assess and manage these issues.

You should carefully consider and document transactions and the commercial business drivers.

Some of the more complex business disposals that may require additional tax governance include:

- earn-out arrangements;

- scrip-for-scrip rollovers;

- share buy-backs and capital reductions;

- business restructuring;

- listing on a stock exchange;

- exit from a consolidated group;

- the use of a demerger to facilitate the disposal of the business; and

- multiple events and transactions that occur just before or on the date of the business disposal.

Tip!

If you are thinking of selling your business or disposing of part of your business, it is important to talk to your tax adviser.

Transferring your business to family members

Transferring control of your business to family members may involve restructuring your business operations, such as:

- changes to the share structure;

- changes to the trustee and appointor of a trust or changes to beneficiaries;

- changes to partnership structures; or

- transferring assets to family members via the creation of trusts or other new entities.

All these events have legal and tax implications that you need to carefully consider.

You should fully document any significant changes to your business structures or operations (including any asset disposals), along with their tax impact. Ensure you properly document information on your assets, such as acquisition date and cost base, improvements and any valuations. This will also ensure that any subsequent disposals of the assets can be treated correctly for tax purposes.

For example, when you dispose of or transfer your business assets, there will likely be CGT consequences. The sale of a business can also trigger GST liabilities.

Where a pre-CGT asset is involved, you should also understand and document whether the asset has retained its pre-CGT status. Issues for consideration include whether changes in beneficial interest impact the pre-CGT status of the assets or shares.

Example: transferring your business to a family member

As the owner of a successful family business, you prepared a basic succession plan many years ago. Since then, your business has expanded and your children have grown up. Your son now works with you in the business. You would like to see him take over when you retire.

You discuss with your adviser how best to transfer the business to your son and transition to retirement. They explain the tax consequences of the transfer. They also alert you to other options and tax considerations.

You decide to restructure your business as a family trust. Then you can still have some control of the business while reducing your involvement in the day-to-day operations.

As you have decided on your current strategy, you update your succession plan and document the tax consequences. Once the business is transferred, you retain documentation evidencing the transactions that have tax impacts. You can now ensure you reflect this correctly in your tax returns.

Tip!

If you are planning on transferring your business to one or more family members, talk to your tax adviser.

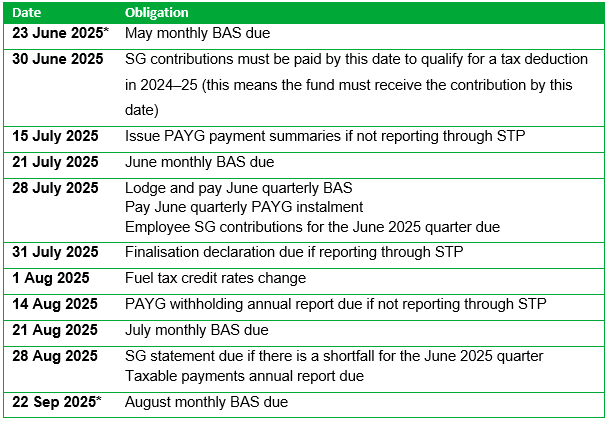

Key tax dates

*This is the next business day as the due date falls on a Saturday or Sunday.

Note!

Talk to your tax agent to confirm the correct due dates for your own tax obligations. For example, you may have more time to lodge and pay if impacted by COVID-19 or a natural disaster.