New Law

Small business instant asset write-off

The Bill extending the $20,000 threshold for the instant asset write-off until 30June next year (which we mentioned in the November 2025 TaxWise) is now law.

This means that an eligible small business can deduct in the current income year (2025-26) the full cost of an eligible depreciating asset purchased after 30 June last year if:

- it costs less than $20,000; and

- is first used, or installed ready for use, before 1 July this year.

An eligible small business may also be able to claim an outright deduction for expenditure on existing depreciating assets that is less than $20,000.

Your business is an eligible small business if its annual aggregated turnover is less than $10 million AND it uses the simplified depreciating rules.

If the cost of a depreciating asset is $20,000 or more, the asset must be placed into the small business pool.

Tip!

Talk to your tax adviser if your business intends to acquire a depreciating asset, or spend money on an existing asset, before 1 July this year.

Payday super

Talk to your tax adviser if your business intends to acquire a depreciating asset, or spend money on an existing asset, before 1 July this year.

Tip!

Talk to your tax adviser as soon as possible about the Payday super reforms and how they will affect your business. 1 July 2026 is less than 5 months away!

GST measures

The GST measures mentioned in the November 2025 TaxWise are also now law. Briefly, the measures will:

- where input tax credits (ITCs) should have been attributed to an earlier tax period but were not, allow the taxpayer to choose to attribute ITCs to the earlier period or a later period;

- allow the ATO to determine the tax period to which an ITC for a creditable acquisition is attributable – if the ATO makes such a determination, the taxpayer only ceases to be entitled to the input tax credit if it has not been taken into account in a GST assessment within four years after they were required to lodge the GST return for the tax period to which the input tax credit is attributed (see below for more about the expiry of GST credits); and

- allow an income tax deduction for the amount of GST payable by way of reverse charge.

Proposed Changes

A Bill introduced into Parliament towards the end of November last year proposes to:

- streamline the choice of fund process during employee onboarding. The amendments provide greater flexibility for when an employer, or their agent, may request details of an employee’s stapled superannuation fund from the ATO, so the employer, or their agent, can provide those details to the employee during onboarding to inform the employee’s choice of fund; and

- increase the maximum amount of WET producer rebate claimable by eligible wine producers, or a group of associated wine producers, from $350,000 to $400,000 per financial year, from 1 July 2026.

Tip!

If you think any of these measures will affect your business, talk to your tax adviser.

What is the ATO Saying?

GST credits

If your business is registered for GST, it can claim GST credits for the GST included in the price of goods and services it buys.

If something is bought for both business and private use, the GST credit needs to be apportioned so only the business use is claimed. For example, if you buy a car for ride-sourcing, you work out the percentage you use it for business purposes and only claim a GST credit on that amount.

You may be able to use annual private apportionment to account for the private portion of business purchases. This means the full GST credits are claimed in the relevant monthly or quarterly business activity statement (BAS), and then a single adjustment is made at the end of the year.

Remember GST credits cannot be claimed for purchases:

- incurred before your business registered for GST;

- where your business does not have a tax invoice;

- that were cancelled or reversed; or

- that do not have GST in the price (such as bank fees).

GST credits expire if not claimed within the 4-year time limit

GST credits will expire if not claimed within the 4-year credit time limit. This is generally 4 years from the due date of the original BAS in which your business could have claimed them. (A 4-year expiry period also applies to fuel tax credits.)

Lodging an amendment request or voluntary disclosure doesn’t preserve credit entitlements. The ATO needs to process your business’ amendment and include it in its assessment within the 4-year credit time limit, otherwise the credits expire.

Once credits expire, the ATO has no discretion or ability to amend an assessment to include those credits.

Your business needs to:

- keep accurate records to support the claims – penalties may apply if your business claims credits it is not entitled to;

- actively manage the risks of expiry of credits if you identify a mistake by considering the available options;

- expect additional scrutiny if it seeks to change long-standing positions to uplift GST recovery, for instance where an apportionment methodology is changed for periods to increase the rates claimed – this will likely take the ATO longer to review and it may need further information, so that should be factored into your business’ timeframes.

Available options

If your business is under current compliance or assurance activity, you should discuss the options available to preserve credit entitlements with the ATO case team as early as possible. It takes time to consider these requests and the ATO may require supporting evidence.

If credits are near expiry, instead of writing to request an amendment, you should consider:

- claiming the credits in your business’ next BAS that’s still within the 4-year credit time limit – these amounts may be subject to future review;

- requesting the amendment by lodging a revised BAS for the tax period to which the credits are attributable. Revised BAS requests are generally processed faster than amendment requests in other forms;

- lodging a valid objection against the assessment for the period to which the GST credits are attributable before the end of the 4-year credit time limit. This should be a last resort and is only appropriate in certain circumstances.

Differences between the 4-year credit time limit and the period of review

The 4-year credit time limit is different to the period of review. The period of review is the period the ATO can amend an assessment, generally 4 years from when the relevant BAS is lodged. The ATO can, however, extend the period of review by agreement.

The 4-year credit time limit for GST credits (and fuel tax credits) applies more strictly. If credits have expired, the ATO is unable to amend assessments to include these credits, even if the period of review is still open. This means there may be situations where the ATO amends for overpaid or underpaid GST or overclaimed credits, but additional credits can’t be included in an amended assessment. So, it’s important to make sure any credit entitlements are claimed within the 4-year credit time limit.

Tip!

Talk to your tax adviser if you think your business is entitled to GST credits (and/or fuel tax credits) which it has not claimed.

Electric vehicles and FBT

Your business does not pay fringe benefits tax (FBT) if it provides private use of an electric car that meets all the following conditions:

- the car is a zero or low emissions vehicle;

- the first time the car is both held and used is on or after 1 July 2022;

- the car is used by a current employee or their associate (such as a family member);

- luxury car tax (LCT) has never been payable on the importation or sale of the car - if your business purchases an electric car second hand, you need to determine if it was subject to LCT at any time in the past.

Benefits provided under a salary packaging arrangement are included in the exemption.

If your business is not eligible for the exemption, for example the car doesn't meet the conditions of a zero or low emissions vehicle, it may need to pay FBT for the private use of the car.

Zero or low emissions vehicle

A vehicle is a zero or low emissions vehicle if it satisfies both of these conditions:

- it is a battery electric vehicle, hydrogen fuel cell electric vehicle or plug-in hybrid electric vehicle. This doesn't include hybrid vehicles that are only fuelled by liquid petrol;

- it is a car designed to carry a load of less than one tonne and fewer than 9 passengers (including the driver).

Motorcycles and scooters are not cars for FBT purposes and don't qualify for the exemption, even if they are electric.

“Held and used” the electric car

The practical effect of this requirement is that the electric car must be used for the first time on or after 1 July 2022 – even if it was held before this date.

An electric car is “held” when it is:

- owned (includes cars acquired under hire-purchase arrangements);

- leased (or let on hire); or

- otherwise made available by another entity.

An electric car is considered “used” when it is used or available for use by any entity or person.

Associated car expenses

The following car expenses are exempt from FBT if they are provided for an eligible electric car:

- registration;

- insurance;

- repairs or maintenance;

- fuel, including the cost of electricity to charge electric cars.

The FBT on any items that aren’t exempt car expenses may be reduced if the expenditure would have been deductible to the employee if they incurred it themselves. This is called the “otherwise deductible rule”.

Home charging station

A home charging station is not a car expense associated with providing a car fringe benefit for electric cars. However, it may be a property fringe benefit or an expense payment fringe benefit.

Cost of electricity to charge electric cars

It can be difficult to work out the cost of electricity when an employee charges an electric car at home. The ATO therefore allows an employer to use the shortcut electric vehicle (EV) home charging rate in certain circumstances.

For zero or low emission cars, the EV home charging rate is 4.20 cents per kilometre. If the EV home charging rate is used, commercial charging station costs cannot be included unless you can accurately determine the percentage of the car's total charge based on the type of charging location. Make sure you keep the necessary records to substantiate how you determined the cost of electricity used to charge the electric car.

If the car is a plug-in hybrid electric vehicle (PHEV) and runs on a combination of electricity and petrol, the ATO provides a simplified method for calculating electricity costs when the car is charged at an employee's or individual's home. Otherwise, to work out the cost of the electricity used to charge an exempt PHEV, you need to calculate the actual electricity expenses.

Make sure you keep the necessary records to substantiate how you determined the cost of fuel including electricity used to charge and run the PHEV.

Reportable fringe benefits

Although the private use of an eligible electric car, including the associated expenses, is exempt from FBT, it is still a reportable fringe benefit.

This means, you will need to work out:

- the notional taxable value of the benefits associated with the private use of the exempt electric car;

- whether the benefit amount needs to be reported.

Tip!

Talk to your tax adviser if you are unsure whether your business needs to pay FBT on an electric car provided to an employee.

Stock for private use

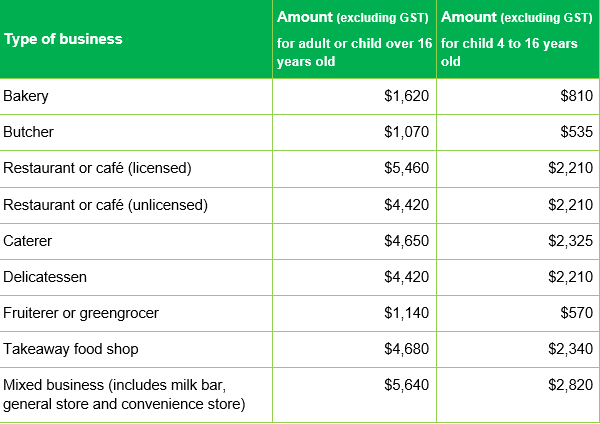

Business proprietors in certain industries are likely to use trading stock for private purposes. This has tax consequences. To assist taxpayers in the relevant industries – those that have as trading stock a range of small items or ingredients, usually of low value, are not suited to inventory systems and have a high turnover of items, often for cash – the ATO publishes annual standard values (excluding GST) that it will accept as estimates of the value of goods taken from trading stock for private use. The industries are: bakery, butcher, caterer, delicatessen, fruiterer/greengrocer, mixed business (e.g. milk bar, general store and convenience store), restaurant/cafe and takeaway food shop.

The ATO has published the standard values for 2025-26 – see the table below. The ATO recognises that greater or lesser values may be appropriate in particular cases. Taxpayers may be able to justify a lower value for goods taken from stock than that shown in the table. In that case, the lower amount should be used. Where the value of goods ex-stock would be significantly greater, the actual amount should be used.

Small Business Superannuation Clearing House is closing

The Small Business Superannuation Clearing House (SBSCH) will be closed permanently from 1 July 2026 as part of the Payday Super reforms. It is not accepting new registrants.

If your business is an existing registered user, it can continue using the SBSCH until 11:59 pm AEST on 30 June 2026. After this time, it will no longer be available and can't be used to make payments or download records.

If your business is an existing registered user of the SBSCH, you need to:

- choose an alternative payment method;

- switch to the new method as soon as possible, before 1 July 2026;

- download your business’ super records from the SBSCH before 1 July 2026.

Alternative payment methods

Your business’ existing payroll software may already include super functions you can use to pay employees' super guarantee (SG). Alternatively, you can look for payroll software and service providers in the ATO’s SuperStream Product register.

Some large super funds may also have online payment services your business can use, or you could use a commercial Clearing House. You send a single electronic payment to the clearing house with all your employees' super contribution data, and the clearing house does the rest.

Contrived property development arrangements

The ATO is currently reviewing certain property development arrangements between related parties involving long-term construction contracts. The arrangements appear to be designed to create an artificial mismatch between the recognition of income from the property development activity and deductions claimed for the costs of development, such that tax on the profits may be indefinitely deferred. The losses generated are utilised within the group to obtain a tax advantage.

In these arrangements, a special purpose developer entity (developer) is interposed between an entity that owns the land being developed (landowner) and another entity undertaking building and construction works on the land (builder). The interposition of the developer artificially separates the landownership and development activities which are, in substance, a single economic activity of property development.

Typically, the terms of the contract deliberately provide that the developer does not derive any income for managing and delivering the development until the project is completed. In addition, the developer exists in form only, and it appears that the services provided to the landowner are all outsourced to the builder and funded by another party.

The losses (arising from the deductions claimed progressively for construction costs while the recognition of income is deferred) are then offset against other income earned by the developer or used to offset other income of the economic group.

While minimal to no tax is paid, there can be significant growth in the wealth of the economic group, and in some cases this wealth is subsequently extracted by individual controllers of the group for their personal benefit.

The ATO’s concerns about this arrangements are outlined in a Taxpayer Alert issued on 14 January.

Tip!

If your business is currently involved in, or considering entering into, an arrangement of this nature, you should talk to your tax advisers.

Fuel tax credits

The excise duty rates for fuel and petroleum products increased on 2 February. For example, the rate for petroleum condensate, stabilised crude petroleum oil and topped crude petroleum oil increased from $0.516 per litre to $0.526 per litre.

Here is a link to the new rates - https://www.ato.gov.au/businesses-and-organisations/gst-excise-and-indirect-taxes/excise-on-fuel-and-petroleum-products/excise-duty-rates-for-fuel-and-petroleum-products

Remember to keep clear records of your fuel purchases and how fuel is used in your business.

Simplified methods

If your business claims less than $10,000 in fuel tax credits each year, it may be able to use a simplified method to calculate fuel tax credits.

For example, if your business uses a heavy vehicle and claims less than $10,000 in fuel tax credits each year, it can use the basic method for heavy vehicles. If your business operates auxiliary equipment, it can use a percentage that the ATO has set to work out how much fuel is used for powering this equipment and when the vehicle is off public roads.

If you are a farmer and your business or residential address is in one of the identified impacted postcodes, and you have a lodgment and payment deferral for that period, you may be able to use the simplified methods for calculating fuel tax credits, regardless of the amount you claim each year.

Simplified record-keeping

Your business can use the following records to substantiate claims of less than $10,000 per year:

- contractor statements – where an amount for fuel used in the performance of services is deducted from the amount payable for the services;

- financial institution statements (such as business or personal credit or debit accounts) – where only the dollar amount is displayed on the statement;

- point-of-sale dockets – where the docket either does not itemise the quantity of fuel dispensed or the quantity is illegible;

- fuel supplier statements or invoices – where only the dollar amount is displayed on the statement.

These records can be used if your business can:

- show the quantity of fuel was used in your business during the period, for example by reference to the type of vehicles and equipment used in the business;

- reasonably demonstrate (if the relevant record is lost), by reference to records from prior or later periods, the quantity of fuel used in your business.

This method can be used for all past and future BAS periods.

Tip!

Your tax adviser can help your business claim the correct amount of fuel tax credits.

Substituted accounting periods

An entity's accounting period is ordinarily the 12-month period ending on 30 June. However, your business can apply to the ATO for permission to adopt an alternative annual accounting period (known as a “substituted accounting period” or SAP).

When applying for a SAP, the business must provide:

- a reason for requesting a SAP; and

- supporting evidence.

The ATO accepts retrospective or out-of-date applications in limited circumstances.

SAPS are granted where your business can demonstrate its circumstances take the case out of the ordinary run. These circumstances may include:

- the need to synchronise balance dates with the controlling entity of the economic group or your business’ holding company;

- if your business has just exited from an income tax consolidated group, the wish to align your business’ balance date with that consolidated group because your business’ accounting systems are already set up to meet the former income tax consolidated group’s reporting requirements and it will be too costly to adjust those systems to a new balance date;

- an ongoing event, industry practice, business driver or other ongoing circumstance that makes 30 June impractical as a basis to calculate taxable income. This would include difficulties with ascertaining inventory for stock valuations, and having multiple financial reporting requirements (for example, a franchise to a franchisee).

Circumstances generally not outside the ordinary run include:

- strata or owners corporations wishing to align their balance date with their audit date;

- companies wishing to align their balance date with a change of company financial year election sent to the Australian Securities & Investment Commission.

Lodging an income tax return with a SAP

Taxpayers who have been granted leave to adopt a SAP must meet the following lodgment requirements:

- individuals, partnerships and trusts – the due date for lodgment is the last day of the fourth month after the close of the accounting period;

- companies and super funds (excluding not full self-assessment taxpayers (NFSA)) – the due date for payment is the first day of the sixth month after the close of the accounting period;

- companies and super funds (excluding NFSA) – the due date for lodgment is the fifteenth day of the seventh month after the close of the accounting period.

Transitioning to a SAP

When a SAP is adopted, the end date of the accounting period changes. This results in a transitional period of more or less than 12 months. An income tax return for the transitional period must be lodged.

The ATO will determine and notify your business of the transitional period when it approves the SAP.

New accounting period

When your business has adopted a SAP, the new accounting period will involve either late or early balancing in relation to a 30 June year end.

Where a SAP ends on any date between 1 July and 30 November, the SAP is in lieu of the income year ending on the preceding 30 June – this is a “late” balance date.

Where a SAP ends on any date between 1 December and 31 May, the period adopted is in lieu of the income year ending on the succeeding 30 June – this is an “early” balance date.

What tax return form to use

A tax return should be prepared by using the form for the year in lieu of which the SAP has been adopted. For example, if your business adopted a SAP ending 31 December 2025, it is an early balancer. The transitional period is therefore in lieu of the following income year ending 30 June, ie the year ended 30 June 2026, and the tax return should be prepared using the 2026 Company tax return form.

If the relevant form has not been produced by the date your business wants to lodge, it must use the most recently available tax return form, whether lodging electronically or by paper.

If your business is transitioning to a SAP, it must lodge a paper form if it is not the entity's first tax return and it is lodging before next year's tax time stationery is released.

Franking period

The transitional period will affect your business’ franking period.

For a corporate tax entity that is not a private company, the franking period depends on the length of its income year. The franking period is different for an early or late balancing corporate tax entity that has adopted a SAP.

Tip!

Your tax adviser can help your business apply for a SAP and prepare its tax returns.

Keeping your business details secure and up to date

Your business must maintain its Australian business number (ABN) details. Details must be updated with the Australian Business Register (ABR) within 28 days of becoming aware of changes.

Regularly reviewing who has access to your business’ tax and business information helps protect your business from fraud or an identity security event. Outdated or incorrect details can make your business vulnerable to security risks.

Businesses may also hold significant taxpayer information. If this data is accessed in an identity security event, it could lead to a serious data breach, affecting you and your business.

Who can access a business’s tax information

Several people and roles may have access or manage a business’s tax details:

- authorised contacts – people officially allowed to speak to the ATO on behalf of the business (with listed addresses and phone numbers);

- ABR associates and contacts – roles linked to the business’s ABN, such as public officers. They have limited access and can only interact with the ATO in specific ways. Certain associates and contacts are considered the principal authority of the business;

- RAM administrators and users – those who can access online services on behalf of your business, for example, Online services for business and the ABR;

- Access Manager permissions – lets you manage which functions others can access on behalf of your business;

- client-to-agent linking – registered agents nominated to act on behalf of the business. These agents would have access to all information on the business held in the ATO’s records.

It’s important to review who has access for each entity and update these details when necessary.

When to contact the ATO

You should contact the ATO as soon as possible if you notice that someone has access to your business’s tax information but was not officially nominated as one of the following:

- authorised contact;

- ABR associate and contacts;

- RAM authorisation;

- assigned permissions in Access Manager.

You should also contact the ATO as soon as possible if business details have been changed without your knowledge, such as updates to your business’ bank account, address or phone number.

Regularly review and update your business details to protect your business and meet legal obligations.

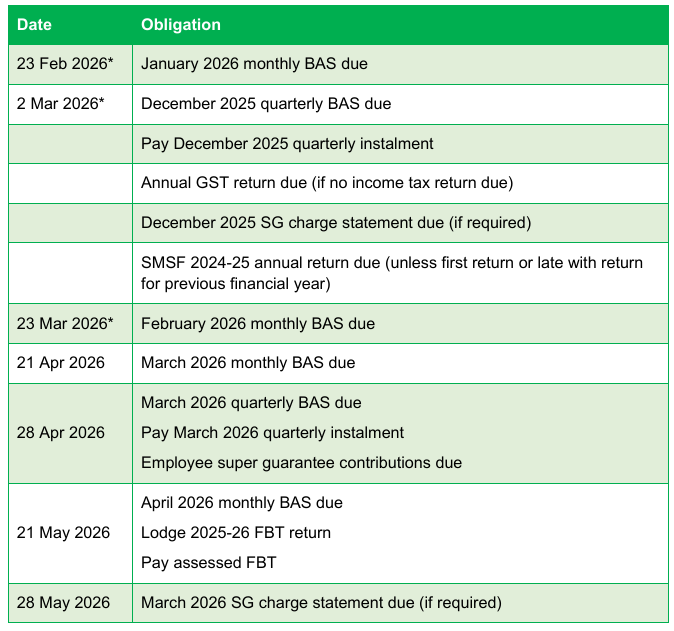

Key tax dates

Note!

Talk to your registered tax agent to confirm the correct due dates for your own tax obligations. For example, you may have more time to lodge and pay if impacted by a natural disaster.

DISCLAIMER

TaxWise® News is distributed by professional tax practitioners to provide information of general interest to their clients. This document does not take into account the specific circumstances of any person and does not constitute professional advice. Readers should not rely on the information contained in this document as advice for any matter, but should make their own assessment and evaluation, undertake investigation and enquiries and seek professional advice to enable them to make any decision concerning their own interests.