From The ATO

The countdown is on for Payday Super!

Yes, Payday Super is less than three months away. We’ve talked about it in previous editions of TaxWise. If you have missed the articles, Payday Super means that employers will make a super contribution for eligible employees each payday (whether weekly, fortnightly or monthly), instead of quarterly.

Here are a couple of useful tips.

Plan your cash flow

Moving from quarterly payments to paying super each payday may affect your cash flow rhythm. This is especially important in July, because you may have your:

- usual April to June quarterly super payment;

- first Payday Super payments (which could be four extra payments if you pay your staff weekly).

Make a plan to manage your cash flow.

Find a new provider as the SBSCH is closing

The Small Business Super Clearing House (SBSCH) will close permanently on 1 July.

Look for an alternative provider now. Don’t wait until 1 July. Taking action now will save you time later and set your business up for success.

Tip!

Talk to your tax adviser or accountant if you are concerned about the transition to Payday Super.

Late payment offset will no longer be available

Currently, employers who make a late super guarantee (SG) payment, can lodge a super guarantee charge (SGC) statement and use the late payment offset (LPO) to reduce their SGC liability by amounts paid late to a fund.

With Payday Super being introduced, this will no longer be available. The last time you can use LPO is for the quarter ending 31 March 2026. Super for this quarter is due by 28 April 2026 and you can claim the LPO when lodging an SGC statement for any late payments made up to and including 30 June 2026.

On 1 July 2026, Payday Super starts and you will pay super for each payday. If you have an SG shortfall for the quarter ending 30 June 2026, SG payments made between 1 to 28 July 2026 will first be used to reduce this shortfall before being applied to payday super amounts. In payday super, late payments will automatically be applied under the law to the oldest outstanding payday super amount.

How to nail your record keeping

Good record keeping helps you manage your business and cash flow, and ensures you get the right outcome with your business’ tax return.

The following tips can help you get it right. They are based on common record-keeping errors seen by the ATO.

- Keep accurate records of all cash and electronic transactions.

- Reconcile cash and EFTPOS sales regularly (by ensuring payments recorded internally match external records) and enter the amounts into your main business accounting software system. Depending on your business, this may be daily, weekly or monthly.

- Check for mistakes if things don't add up.

- For expenses that are for both business and private use, work out and record the business portion accurately.

- If you have used trading stock for private purposes, remember to account for the stock as if you’ve sold it and include the value in your business’s assessable income to ensure your cost of sales figures are accurate.

- Ensure you have sufficient records to substantiate business expenses claimed as tax deductions.

- Don't use estimates to prepare your tax returns and business activity statements (BAS). Ensure you have complete and accurate records to substantiate the information you include in them.

- You generally need to keep most records for five years – from when you prepared or obtained the record, or completed the transaction or related acts, whichever is later. For example, if your business buys a plot of land, you need to keep the record for five years after the land is handed over to you. However, if you then decide to build a new property on the land and that takes two more years, you will need to keep the record for at least seven years.

- You should also keep records long enough to cover the end of the period of review.

- If your business incurs a tax loss – or a capital loss that can be offset against capital gains, remember you need to keep records related to how you determined and worked out that loss for five years or the end of the period of review for the income year when the loss is fully deducted, whichever is later.

- If you are paying contractors to provide certain services on your behalf, remember to keep accurate and detailed records. This way, you can easily prepare your total payments to each contractor at the end of the year to help you complete your taxable payments annual report (TPAR).

- If you are claiming GST credits, set aside your GST in a separate ledger account to make your record keeping and calculations easier.

- If you had PAYG amounts withheld from payments to your business (for example, because of a voluntary agreement or labour hire arrangement), ensure your payer gives you a PAYG payment summary. You may need it to substantiate any PAYG credits you later claim in your tax return.

Digital record-keeping

There are advantages in keeping business records digitally. If, for example, your business uses a commercially-available software package, it may help the business:

- keep track of business income, expenses and assets as well as calculate depreciation;

- streamline its accounting practices and save time so you can focus on the business;

- automatically calculate wages, tax, super and other amounts for activity statement and other purposes;

- meet Single Touch Payroll (STP) reporting obligations;

- back up records using cloud storage to keep records safe from flood, fire or theft.

If your business uses cloud storage, either through accounting software or a separate service provider, for example, Google Drive, Microsoft Onedrive or Dropbox, you should ensure:

- the record storage meets the record-keeping requirements;

- you download a complete copy of any records stored in the cloud before you change software provider and lose access to them.

eInvoicing storage

Regardless of your business’ eInvoicing software or system, you are responsible for determining the best option for storing business transaction data. You should:

- ensure that the process meets the record-keeping requirements;

- discuss the options with the software provider;

- talk to your business adviser, if necessary.

Tip!

Not sure what records you should keep and how long you should keep them for? Talk to your tax adviser.

Check your PAYG instalments

Now is a good time to check that your business’ PAYG instalments still reflect the expected end of year tax liability.

If your business’ circumstances have changed and you think you will pay too much (or too little) in instalments for the year, the instalments can be varied on the activity statement for the March 2026 quarter. Instalments can be varied multiple times throughout the year. The varied amount or rate will apply for the remaining instalments for the tax year or until another variation is made.

If your business is affected by a natural disaster, the ATO has the discretion not to apply penalties or charge interest to varied instalments if you have made your best attempt to estimate your end of year tax liability.

If an amount or rate is varied online, activity statements and instalment notices will be issued electronically and not in paper form. You will need to consider this when deciding how to lodge, revise and vary future activity statements and instalment amounts.

Tip!

Your tax adviser or BAS agent can help you with your activity statements and tax returns.

Car expenses – logbook method

If you are a sole trader and you use the logbook method for claiming car expenses, you need keep the following types of records:

- odometer records for the start and end of the period you own the car during the income year you rely on the logbook;

- proof of purchase price, or a new lease agreement and lease payment records;

- decline in value calculations;

- fuel and oil receipts, or records of a reasonable estimate of these expenses, based on odometer readings;

- if you have an electric or plug-in hybrid car, receipts from commercial charging stations or evidence showing you incurred additional electricity costs to charge the car at home, such as an electricity bill and the calculation of the direct cost to recharge – you cannot claim any commercial charging costs if you use the home charging rate of 4.2 cents per kilometre for a reasonable estimate of home charging, based on odometer readings. If the car is a plug-in hybrid, a specific formula must be used to calculate home charging expenses;

- registration and insurance – evidence of payment;

- servicing, repairs and tyres – evidence of payment.

Do you need a new logbook?

You can keep the same logbook for your car for five years, but there are circumstances where you may need a new one during that period. Relying on a logbook that no longer represents work-related travel may result in you claiming more, or less, than you are entitled to.

A new logbook may be required when you:

- change address;

- have changes to your pattern of use of the car for work purposes.

If you use the logbook method for two or more cars, you need to keep a logbook for each car and make sure they cover the same period.

If you purchase a new car during the income year and want to continue relying on your previous car's logbook, you must make a nomination in writing. The nomination must be made before you lodge your tax return and state:

- you are replacing your original car with a new car; and

- the date that nomination takes effect.

Compare your business with industry standards

You can compare your business's performance against others in your industry by using the ATO’s small business benchmarks.

The ATO states that its benchmark methodology has been verified as statistically valid by an independent organisation and is consistent with international approaches. If you want to know more about the methodology, you can visit the ATO website - click here

The benchmarks:

- are based on the biggest data set available;

- account for businesses with different turnover ranges across 100 industries;

- are published as a range to recognise the variations between businesses and different locations and circumstances.

The ATO allocates business data to a business type based on a combination of:

- business industry code;

- the main business activity listed on the tax return;

- the trading name label of the business.

The ATO has published on its website the latest performance benchmarks, based on information reported on tax returns for the 2023–24 income year, for approximately 100 industries. There is a good chance that the industry your business is part of is covered.

Tax Tips

How to reduce your tax bill

We are getting near the end of the tax year (30 June), so you might want to consider ways to reduce your business’ tax bill.

The two simplest ways to do this are to reduce assessable income or increase deductible expenditure. Either way, the business’ taxable income (and thus the amount of tax payable) is reduced.

If your business reports income on a cash basis, one way to reduce assessable income for the current income year is to delay sending an invoice to a customer until after 30 June. Of course, cash flow issues may dictate otherwise.

If you are in the process of selling property and the profit will be taxable as a capital gain, you could defer the sale until the next income year – but remember that the liability to pay capital gains tax (CGT) arises when you exchange contracts and not on settlement.

You can increase deductible expenditure by bringing it forward from the next income year to the current income year. This is particularly useful where an immediate deduction is available — for example, for depreciating assets costing less than $20,000 if you are a small business which uses the simplified depreciation rules, start-up costs and certain prepaid expenses.

Charitable donations are a good way to increase your deductions. If you are not sure if a donation will be deductible, you can check the deductibility status of charities at https://www.abn.business.gov.au/Tools/DgrListing. In certain circumstances, a deduction is available where trading stock is donated. Don’t forget to ask for a receipt.

What are the benefits?

If you are a sole trader or a partner in a partnership, the benefits of reducing your taxable income could include:

- reducing your marginal tax rate, for example, from 37% to 30%, or from 30% to 16%; and

- avoiding liability for the Medicare levy surcharge (MLS) (at least 1% of your income for MLS purposes) if you do not have appropriate level of private health insurance hospital cover.

In addition, the lowest marginal rate for individuals will decrease from 16% to 15% from 1 July this year, so there is a small benefit in taking steps that will reduce your taxable income this year but increase it for next year.

Tip!

As the end of the income year approaches, talk to your tax adviser about ways to minimise your tax bill.

Instant asset write-off

As things stand, the instant asset write-off threshold for small businesses (aggregated turnover under $10 million) will drop from $20,000 for the current tax year (2025-26) to $1,000 for the next tax year (2026-27) starting on 1 July. So if you intend to acquire a

depreciating asset valued at between $1,000 and $20,000, you should consider making the acquisition before 30 June so you can write off the total amount this tax year.

Having said that, it would not be a surprise if the Government extends the $20,000 threshold for at least another year. If the Government does this, it will probably be announced in the 2026-27 Federal Budget which is to be handed down on Tuesday 12 May.

FBT Issues

It's FBT tax time – are you ready?

Has your business provided employees (or associates of employees such as a spouse or child) with any perks or extras, like work vehicles, held any social events, or even paid for their personal expenses? You may need to lodge a fringe benefits tax (FBT) return and pay any FBT owed.

The FBT year runs from 1 April 2025 to 31 March 2026, so, if your business has provided any perks during this time (or even think it might have), now's the time to sort it out.

These four key steps will assist your business to confidently meet its FBT obligations and help it stay compliant.

Identify the fringe benefits

Start by working out what employee perks have been provided and what type of fringe benefit they are. Don't skip this step – it's essential to help you understand what records must be kept and to calculate the liability correctly. For example, ask employees if have they taken the work vehicle on a weekend getaway. If so, it could mean FBT applies.

Determine the taxable value

Use the relevant calculation methods to work out the taxable value for each fringe benefit your business provides. This will help you calculate the total taxable amount and FBT liability correctly.

Keep accurate records

Ensure the right records to support your business’ FBT position are kept. The type of records that must be kept will depend on the fringe benefit provided. The records should also show calculations and support any exemptions or concessions claimed.

Lodge, pay and report

Make sure to lodge the FBT return (and pay any outstanding FBT) by 21 May 2026. If your business uses a tax agent, it may have until 25 June 2026.

Your business may also need to report any reportable fringe benefits amounts for employees by 14 July 2026.

Common errors

Getting FBT right the first time can help avoid unexpected liabilities, penalties and additional paperwork. Many mistakes are avoidable, so be aware of some of the common issues that will attract the ATO’s attention, including:

- lodging a nil FBT return when fringe benefits were provided;

- treating private use of work vehicles as business use or failing to report it;

- incomplete or invalid records to support exemptions or concessions used, or to show how the taxable value of benefits was calculated;

- incorrect reporting of employee contributions to reduce FBT liabilities or reporting at the incorrect label in the income tax return.

Don't need to lodge?

If your business is registered for FBT but its FBT liability is nil, a Fringe benefits tax – notice of non-lodgment must be still be sent to the ATO.

Providing perks to employees

If you provide work vehicles or other perks to employees – even if they're provided occasionally – your business may be providing a fringe benefit. This means your business could have FBT obligations.

Many businesses provide fringe benefits without realising it. Fringe benefits are non-cash perks provided to employees (or their family members or associates), on top of their wage or salary.

The most common example is providing a work vehicle that's used for personal purposes, which includes when it's garaged at an employee's home. If employees use work vehicles privately, take the time to understand your obligations so you can lodge correctly and stay compliant.

Electric car exemption eligibility

Since 1 April 2025, plug-in hybrid electric vehicles (PHEVs) are no longer eligible for the electric car exemption, unless your business meets the specific eligibility requirements. This means your business may now have an FBT liability, if you've continued providing a PHEV for employees' personal use.

Shortcut home-charging method

If employees charge PHEVs at home, your business may be able to use the shortcut method which makes it easier to calculate home-charging electricity costs. Even if eligible to use that method, your business can continue to use the actual electricity costs.

FBT and car parking

Your business will provide a car parking fringe benefit to an employee if on any day all the following occur:

- your employee parks their car (or a car your business provides them) in a place that you own, lease or control (your business premises) which is at or near their primary place of employment;

- the business premises are within 1 kilometre (by the shortest practicable route) of a commercial parking station that charges an all-day parking fee greater than the car parking threshold ($11.03 for the 2025-26 FBT year) on both the first day of the FBT year (1 April) and the day the benefit is provided;

- the car is parked for more than 4 hours between 7.00 am and 7.00 pm;

- the employee drives their car between home and work, or vice versa, at least once;

- your business is not exempt from car parking fringe benefits.

Exemptions from car parking fringe benefits

Your business will not have to pay FBT for providing an employee with car parking, if any of the following apply:

- the employee has a disability – the employee must both be legally entitled to use a parking bay marked with the international symbol of access and have a valid accessibility parking permit displayed on the car;

- your business is a small or medium business (generally aggregated turnover less than $50 million) and the parking isn't provided in a commercial car park. This exemption does not apply if the business is a listed public company or a subsidiary of a listed public company;

- your business is an exempt employer – this category includes registered charities, non-profit scientific institutions, public educational institutions, public or not-for-profit hospitals and public ambulance services (in the case of hospitals and ambulance services, the benefit must be within the employee capping threshold).

If you provide car parking occasionally, it may qualify for the minor benefits exemption if it has a value of less than $300 and it would be considered unreasonable to treat it as a fringe benefit.

Note that car parking benefits provided to an associate of an employee may also be subject to FBT.

Tip!

If your business provides car parking benefits to employees, talk to your tax adviser to see if your business will be liable to pay FBT.

Party-planning for employees

Is your business planning a party for its employees, or thinking in advance about an end-of-financial-year celebration? If so, make sure you consider the FBT implications as the party or celebrations may constitute entertainment-related fringe benefits.

This will depend on:

- the amount spent on each employee;

- when and where the party is held;

- who attends - is it just employees, or are partners, clients or suppliers also invited; and

- the value and type of gifts provided.

Remember to keep all records relating to any fringe benefits provided, including how the taxable value of benefits is calculated.

Tip!

Talk to your tax adviser before holding a party for employees.

FBT issues attracting ATO’s attention

The ATO has published information about what FBT issues attract its attention.

Motor vehicles

Situations that concern the ATO include when employers:

- fail to identify or report car fringe benefits;

- incorrectly apply exemption provisions for vehicles that are not eligible or by treating all travel as business;

- incorrectly claim reductions for these benefits without the appropriate records to support the reduction.

A simple way to work out if a trip is business or private, ask if the employee could claim an income tax deduction if they paid for the costs of using the car.

Things like home to work trips, going and grabbing lunch and picking up the kids up from school are generally all private trips and the employee cannot claim a tax deduction. Those trips are therefore subject to FBT.

Logbook errors

Logbooks need to contain enough detail to clearly demonstrate the usage of the car during the logbook period.

The key details to include are:

- dates the journey started and ended;

- odometer readings at the start and end of each journey;

- kilometres travelled;

- purpose of the journey.

Common logbook errors the ATO sees include:

- insufficient information about the purpose of the journey – simply saying it was a 'business’ journey isn’t enough;

- co-mingled business and private trips listed as one entry;

- discrepancies and inconsistencies – the logbook entries should match the actual travel.

If a logbook is being used, odometer records need to be kept at the start and end of the FBT year.

Employee contributions

Employee contributions are one of the main ways employers can reduce their FBT liability.

Situations that concern the ATO include when employers:

- apply an estimated employee contribution with the intention to reduce their FBT liability to nil, but they don't calculate their liability first - your business needs to identify what type of benefit has been provided and its taxable value by the time the return is due and your business can't work out the FBT liability later and then apply a matching employee contribution afterwards;

- seek to amend past income tax returns, by including employee contributions - once financial statements for a financial year have been finalised, your business can’t discharge a past year FBT obligation through journal entries;

- report employee contributions in their FBT return but don't report the corresponding amount in their income tax return, or reporting at the incorrect label – the ATO looks out for mismatches between the amount reported as an employee contribution on the FBT return and the income amounts on the employer's tax return.

Incorrect reporting may trigger compliance action.

Entertainment

If your business provides employees or their associates with food and drink, gifts or leisure activities (such as Christmas parties and business lunches) your business may have a FBT liability.

The ATO looks out for situations where employers are providing entertainment activities to their employees and the expenses are:

- claimed as deductions in their tax return without correctly reporting and paying FBT;

- classified as sponsorship or advertising where there is an entertainment aspect to the activity.

Car parking valuation

Your business is required to obtain a valuation report to support the calculation of car parking fringe benefits from a suitably qualified valuer and substantiate the market valuation.

The ATO is aware that COVID-19 has affected the rates of commercial parking in many areas, and that market valuations may be impacted as a result.

For car parking, situations that concern the ATO include when the calculation is based on:

- nil market valuations or market valuations that appear to be significantly discounted;

- parking rates that are not representative of commercial parking in the area;

- parking rates that are not supported by evidence.

Nil lodgment

The ATO sees employers lodging nil returns when they haven’t taken the required steps to determine if they have an FBT liability.

Before lodging a nil return, or submitting a Fringe benefits tax – notice of non-lodgment (NAT 3094), it's essential that your business has identified whether a benefit has been provided, determined the taxable value and kept the required records for FBT.

Your business can’t simply lodge a nil return by the due date and work out if you have an FBT liability later. Lodging an incorrect return is subject to penalty.

New FBT year resolutions

To help your business start the new FBT year (commencing on 1 April) on the right foot, here are a few tips.

When providing fringe benefits to employees, your business needs to:

- self-assess its FBT liability for the FBT year;

- lodge an FBT return (if your business has an FBT liability or paid FBT instalments through its activity statements);

- pay the FBT owed by the due date; and

- include the reportable fringe benefits on each employee’s income statement or payment summary (if the total taxable value is more than $2,000).

If your business’ FBT liability for the 2025-26 FBT year was $3,000 or more, you will need to pay four quarterly instalments.

You should also know that:

- there are exemptions and concessions which can reduce the amount of FBT your business pays; and

- errors on the FBT return can be amended or you can make a voluntary disclosure.

Tip!

If your business provides perks to employees, talk to your tax adviser to make sure you comply with the FBT rules.

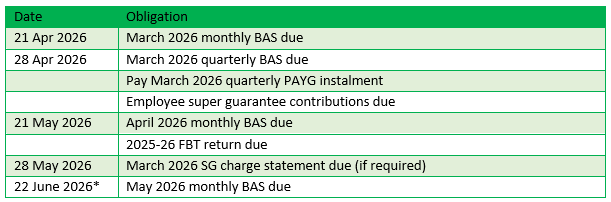

Key tax dates

Note!

Talk to your tax agent to confirm the correct due dates for your own tax obligations. For example, you may have more time to lodge and pay if impacted by a natural disaster and quarterly payers may qualify for a 2-week extension to lodge their March BAS. The due date for FBT returns lodged through a tax agent is 25 June 2026.

DISCLAIMER

TaxWise® News is distributed by professional tax practitioners to provide information of general interest to their clients. The content of this newsletter does not constitute specific advice. Readers are encouraged to consult their tax adviser for advice on specific matters.