Tax Highlights

On Tuesday 12 May, the Treasurer, The Hon Dr Jim Chalmers MP, delivered the 2026-27 Federal Budget, his fifth Budget.

From a tax perspective, this Budget is possibly the most significant in the last 20 years. What stands out?

Capital gains tax – from 1 July 2027, the 50% CGT discount will be replaced by cost base indexation for assets held for more than 12 months, with a 30% minimum tax on net capital gains.

Negative gearing – negative gearing for residential property will be limited to new builds. From 1 July 2027, losses from established residential properties acquired from 7:30PM (AEST) on 12 May 2026 will only be deductible against rental income or the capital gains from residential properties. Excess losses can be carried forward to be offset against residential property income in future years.

Discretionary trusts - from 1 July 2028, trustees will pay a minimum tax of 30% on the taxable income of discretionary trusts. Beneficiaries, other than corporate beneficiaries, will receive non-refundable credits for the tax payable by the trustee.

Tax cut – the Working Australians Tax Offset of $250 will be available to taxpayers who derive income from work (eg salaries and wages and a sole trader’s business income), as from the 2027-28 income year.

Instant asset write-off - the $20,000 threshold for the instant asset write-off for small business will be permanent from 1 July this year.

Loss carry back – for income years commencing on or after 1 July 2026, companies with aggregated annual global turnover of less than $1 billion will be able to carry back a tax loss and offset it against tax paid up to two years earlier.

FBT exemption for EVs - the FBT exemption for zero or low emission vehicles will be phased out between 1 April 2027 and 31 March 2029, to be replaced by a 25% discount from 1 April 2029 onwards.

R&D incentive - from 1 July 2028, various measures will ensure the R&D tax incentive is better targeted, for example by increasing the offset for core R&D expenditure by around 25% to 50% and reducing the intensity threshold from 2% to 1.5%.

Venture capital incentives - the venture capital tax incentives will be expanded from 1 July 2027 to better facilitate venture capital investment and support early stage and growth businesses.

PAYG instalments - from 1 July 2027, small and medium businesses will be able to opt in to reporting and paying PAYG instalments monthly.

Previously announced measures

Standard deduction - employees and certain other taxpayers (but not sole traders) will be able to claim from the 2026-27 income year a standard $1,000 tax deduction for work expenses without needing to supply receipts.

Tax cuts - don’t forget that the tax rate for incomes between $18,200 and $45,000 will be reduced from 16% to 15% from 1 July this year (and from 15% to 14% from 1 July 2027). Further details of these measures can be found below.

Superannuation

Like last year, there were no significant announcements concerning superannuation.

Budget papers

If you want to read the Budget papers, you can find them at budget.gov.au. The tax changes are discussed in Statement 4 (Tax reform for workers, businesses and future generations) which is attached to Budget Paper No 1 (Budget Strategy and Outlook).

CGT and negative gearing reforms

The Government has announced significant reforms to the capital gains tax (CGT) discount and negative gearing, which are intended to support home ownership. The reforms are estimated to increase receipts by $3.6 billion over the five years from 2025- 26.

CGT reforms

From 1 July 2027, the 50% CGT discount will be replaced by cost base indexation for assets held for more than 12 months, with a 30% minimum tax on net capital gains. These changes will apply to all CGT assets, including pre-1985 CGT assets, held by individuals, trusts and partnerships.

For assets held prior to 1 July 2027, but sold thereafter, the 50% CGT discount will apply to the difference between the asset’s value at 1 July 2027 and its cost base, while indexation and the minimum tax will be used to calculate the CGT on gains accruing from 1 July 2027 (the asset’s value at that date will form its cost base). To determine the asset’s value at this date, taxpayers can either seek a valuation or use a specified apportionment formula that estimates the asset’s value based on its average return over the holding period (supported by ATO tools). These transitional arrangements are prospective, applying only to gains that accrue after the start date.

The same approach will apply to assets acquired before the beginning of CGT in 1985. Bringing assets held before 1985 into the CGT regime will improve horizontal equity and enhance the intergenerational equity objectives of the package. At the same time, this approach preserves existing treatment of gains on pre-1985 assets earned before 1 July 2027. Gains on pre-1985 assets earned from 1 July 2027 will be taxed under the new arrangements upon realisation.

To maintain incentives for new housing supply, investors in new residential properties will be able to choose either the 50% CGT discount, or cost base indexation and the 30% minimum tax.

Income support payment recipients, including Age Pension recipients, will be exempt from the 30% minimum tax.

The Budget Papers state that the 30% minimum tax will reduce incentives to defer the sale of assets to periods when other income and marginal tax rates are low. This will support a more consistent taxation of lifetime income by aligning the tax rate on real capital gains with the marginal tax rate faced by the average worker on incomes from $45,000 to $135,000.

The Treasurer said in a media release that further consultation will be undertaken with stakeholders to settle the details for implementation, including the treatment of early‑stage and start‑up businesses given the unique features of the tech and start‑up sector.

Negative gearing reforms

The Government will limit negative gearing for residential property to new builds.

From 1 July 2027, losses from established residential properties will only be deductible against rental income or the capital gains from residential properties. Excess losses will be carried forward and able to be offset against residential property income in future years. These changes will apply to established residential properties acquired from 7:30PM (AEST) on 12 May 2026.

Transitional arrangements will ensure the arrangements for taxpayers who made investment decisions under current settings do not change. Properties purchased or held prior to announcement will be exempt from the changes until disposed of (ie the changes will apply to the new owner). This includes properties where a contract has been entered into but not yet settled.

Properties purchased after 7:30pm (AEST) on 12 May 2026 and before 30 June 2027 may be able to be negatively geared during this period, but not in subsequent years.

Eligible new builds will be exempt from the changes, ensuring the benefits of negative gearing are directed to investment that increases the housing stock. Properties in widely held trusts and superannuation funds will be excluded, alongside targeted exemptions for build-to-rent developments and private investors supporting government housing programs.

Trust reforms

The Government will introduce a 30% minimum tax on discretionary trusts.

From 1 July 2028, trustees will pay a minimum tax of 30% on the taxable income of discretionary trusts. Beneficiaries will still need to declare the income in their tax returns, but beneficiaries, other than corporate beneficiaries, will receive non-refundable credits for the tax payable by the trustee, which can be used to offset current year income tax liabilities.

The Treasurer said in a media release that these reforms won’t change or limit the use of trusts for legitimate reasons, but will more closely align the tax rates for trusts with the rates paid by workers and families who earn a living from wages.

The minimum tax will not apply to other types of trusts that don’t offer the same flexibility as discretionary trusts, such as fixed and widely held trusts (including fixed testamentary trusts), complying superannuation funds, special disability trusts, deceased estates and charitable trusts. Some types of income such as primary production income, certain income relating to vulnerable minors, amounts to which non-resident withholding tax applies, and income from assets of discretionary testamentary trusts existing at announcement will also be excluded.

The Government will provide expanded rollover relief for three years from 1 July 2027 to support small businesses and others that wish to restructure out of discretionary trusts into another entity type, such as a company or a fixed trust.

This measure is estimated to increase receipts by $4.5 billion over the five years from 2025-26.

Tax measures for individuals

Work related deductions

The Government will introduce an instant tax deduction of up to $1,000 from the 2026-27 income year.

Australian tax residents who earn income from work will be eligible for the instant tax deduction and will not need to itemise and claim work‑related expenses if claiming less than $1,000. Individuals who incur work‑related expenses greater than the instant tax deduction can continue to claim their deductions in the usual way – ie, they will need to substantiate all deductions.

This measure applies not only to employees, but to company directors, office holders and religious practitioners who are subject to the PAYG withholding system. Sole traders will not be eligible for the instant deduction.

Charitable donations, union and professional association membership fees and other non‑work‑related deductions can still be itemised separately and claimed on top of the instant tax deduction.

This measure was part of Labor’s 2025 Federal election policies. Draft legislation to implement this measure has already been released.

The instant tax deduction is expected to decrease receipts by $2.4 billion and increase payments by $183.9 million over four years from 2025-26.

Working Australians Tax Offset

The Government will introduce a $250 Working Australians Tax Offset from the 2027-28 income year. The offset will provide a permanent annual tax offset for Australians for their income derived from work, such as wages and salaries and the business income of sole traders, from 1 July 2027.

The Working Australians Tax Offset will increase the effective tax-free threshold for income derived from work by nearly $1,800 to $19,985 (or up to $24,985 for workers eligible for the Low Income Tax Offset). The Government says that this is the largest permanent increase in the effective tax-free threshold since 2012-13.

This measure is estimated to decrease receipts by $6.4 billion over the five years from 2025– 26. The ATO will receive $10 million over five years from 2025– 26 to support implementation of the measure.

Note: Don’t forget that the tax rate for incomes between $18,200 and $45,000 will be reduced from 16% to 15% from 1 July this year (and from 15% to 14% from 1 July 2027).

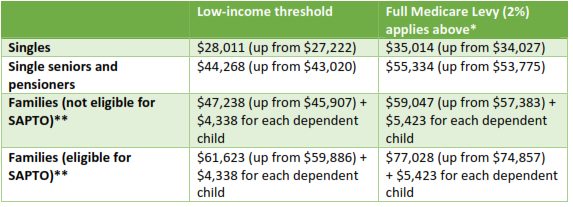

Medicare levy thresholds

The Government announced the Medicare levy low-income thresholds for the 2025-26 income year. They vary depending on whether the taxpayer is eligible for SAPTO (the senior and pensioners tax offset) and whether the taxpayer has dependent children or students.

The new thresholds are set out in the following table.

* The Medicare levy phases in at 10 cents for each dollar above the relevant low-income threshold until the full 2% levy applies. The amounts in this column for 2025-26 are estimated only.

** SAPTO is the senior and pensioners tax offset.

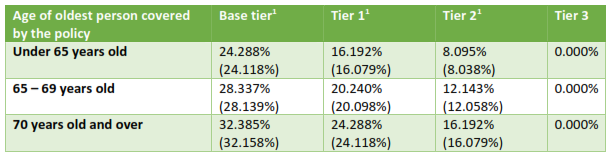

Private health insurance offset

The Budget confirmed the Government's previous announcement in April that the private health insurance offset will be reduced for those aged 65 and over.

On 22 April 2026, the Minister for Health and Ageing, Mark Butler, said that the higher rate offsets for those aged 65 and over will be scrapped from 1 April 2027. Instead, the offset for those aged 65 and over will be the same as for those aged under 65. The changes are expected to save $3 billion over four years from 2026-27 (and $1bn per year ongoing).

The offset percentages for 2025-26 are set out in the table below.

The numbers in parentheses apply to premiums paid on or after 1 April 2026)

The income tiers for 2025-26 are:

Tax deductible donations

The Government will amend the tax law to specifically list the following organisations as deductible gift recipients (DGRs) for gifts received after 30 June 2026 and before 1 July 2031:

- CEW Bean Foundation;

- Council of First Nations Ltd;

- Hakoah Club Ltd (for gifts received after 30 June 2025 and subject to maintaining tax exempt status as a not‑for‑profit sporting organisation);

- Jewish Education Foundation (Vic) Ltd;

- Sydney Harbour Federation Trust;

- Sydney Harbour Foundation Limited;

- Virtual War Memorial Limited.

In addition, the Government has named the Jewish Community Foundation (JCF) and Australian Jewish Funders (AJF) in a ministerial declaration, enabling them to seek DGR endorsement as community charities with the ATO.

Further, the Government will remove the ministerial declaration requirement from the community charity DGR process, reducing red tape for eligible community charities by removing a step in the endorsement process.

$2 minimum limit scrapped

The $2 threshold for claiming a deduction for a donation to a DGR will be scrapped with effect from 1 July 2024 (legislation to implement this measure was introduced into Parliament towards the end of March). So, for example, if you round up your supermarket bill to make a donation to a charity, you will be able to claim a deduction for the additional amount, even if it is less than 50 cents. It may be advisable to keep the supermarket receipt.

PNG Chiefs

The Government will amend the tax law to ensure that income tax exemptions provided by Papua New Guinea for players and staff of the PNG Chiefs National Rugby League team operate as intended.

This will decrease receipts by $5.4 million over four years from 2026-27.

Business tax measures

Small business - instant asset write-off

From 1 July 2026, the Government will extend permanently the $20,000 instant asset write‑off for small businesses. $20,000 is the threshold for the current income year (2025-26).

This means that a small business (aggregated annual turnover under $10 million), that uses the simplified depreciation rules, will be entitled to an instant deduction for the cost of any depreciating asset acquired on or after 1 July this year if it costs less than $20,000. No more wondering in the lead up to the end of the financial year if your business should acquire an asset costing between $1,000 and $20,000 before the end of the year.

Assets valued at $20,000 or more can continue to be placed into the small business simplified depreciation pool.

The provisions that prevent small businesses from re‑entering the simplified depreciation regime for 5 years after opting out will continue to be suspended until 30 June 2027.

This measure is estimated to decrease receipts by $815 million and increase payments by $17.2 million over the five years from 2025-26.

Treatment of tax losses

The Government will allow businesses to carry back losses.

For income years commencing on or after 1 July 2026, companies with aggregated annual global turnover of less than $1 billion will be able to carry back a tax loss and offset it against tax paid up to two years earlier. Loss carry back will apply to revenue losses only and will be limited by a company’s franking account balance.

Similar loss carry back measures were announced in the 2020-21 Federal Budget. Eligible companies were allowed to carry back tax losses from the 2019-20, 2020-21 or 2021-22 income years to offset previously taxed profits in 2018-19 or later income years. The regime was later extended by one year to allow losses from 2022-23 to be carried back as far as 2028-19.

Small start-up companies

The Government will also introduce loss refundability for small start‑up companies. For income years commencing on or after 1 July 2028, start‑up companies with aggregated annual turnover of less than $10 million that generate a tax loss in their first two years of operation will be able to utilise the loss to generate a refundable tax offset. The offset will be limited to the value of fringe benefits tax and withholding tax on wages paid in respect of Australian employees in the loss year.

The Budget Papers state that up to 25,000 new small companies could be eligible for the refundable tax offset each year. Around half of these companies are expected to be able to fully offset their losses while the other half would be able to partially offset their losses. The benefits are expected to flow across sectors, but particularly to the construction and professional, scientific and technical services industries.

The loss carry back and start-up changes are estimated to decrease receipts by $2.3 billion and increase payments by $468.2 million over the five years from 2025-26. The ATO will receive $58.2 million over five years from 2025-26 to support implementation of the measures.

FBT exemption for EVs

The fringe benefits tax (FBT) exemption for electric vehicles (EVs) is to be gradually phased out, to be replaced by a 25% discount.

From 1 April 2029, a permanent 25% discount on FBT will be available for all electric cars valued up to and including the fuel‑efficient luxury car tax threshold, implemented through a 15% rate in the FBT statutory formula.

The following transitional arrangements will be put in place:

- All eligible electric cars will retain the FBT discount rate that was in place when the arrangement commenced.

- All electric cars valued up to and including $75,000 that are provided before 1 April 2029 will continue to be eligible for a 100% discount on FBT, implemented through a 0% rate in the FBT statutory formula.

- Electric cars valued above $75,000 and up to and including the fuel‑efficient luxury car tax threshold that are provided between 1 April 2027 and 1 April 2029 will be eligible for a 25% discount on FBT, implemented through a 15% rate in the FBT statutory formula.

The existing 20% statutory rate will continue to apply for all other cars, including electric cars costing more than the fuel‑efficient luxury car tax threshold.

Reportable fringe benefits will continue to be determined for eligible electric cars as if a 20% FBT statutory formula rate or cost basis method applied.

The fuel‑efficient luxury car tax threshold is presently $91,387, but will inevitably be higher by 1 April 2027.

Better targeting the Research and Development tax incentive

From 1 July 2028, the Government will:

- increase the offset for core R&D expenditure by around 25% to 50%, through a 4.5 percentage point increase in core R&D offset rates;

- reduce the intensity threshold from 2% to 1.5%, enabling more firms that engage in substantial core R&D to qualify for higher offset rates;

- remove eligibility of supporting R&D expenditure for the R&D tax incentive;

- enable growing firms to retain access to the refundable tax offset for longer by increasing the turnover threshold for the highest offset rate from $20 million to $50 million;

- for firms below the $50 million turnover threshold, maintain older firms’ eligibility for the higher offset rate while limiting refundability to firms under 10 years of age;

- lift the maximum R&D tax incentive expenditure threshold from $150 million to $200 million; and

- improve assurance on smaller claims by lifting the minimum expenditure threshold from $20,000 to $50,000, with research activities valued below this amount required to be undertaken with a registered Research Service Provider or Cooperative Research Centre to be eligible for the R&D tax incentive.

This measure is estimated to decrease receipts by $910 million and decrease payments by $1.6 billion over the five years from 2025-26.

Venture capital tax incentives

The Government will expand the venture capital tax incentives to better facilitate venture capital investment and support early stage and growth businesses.

From 1 July 2027:

- the venture capital limited partnership (VCLP) cap on the asset size of the investee business at the time of investment will be increased to $480 million, from $250 million;

- the early stage venture capital limited partnership (ESVCLP) cap on the asset size of the investee business at the time of investment will be increased to $80 million, from $50 million;

- the ESVCLP tax incentive cap on the asset size of the investee business, at which investment returns can be fully tax exempt, will be increased to $420 million, from $250 million; and

- the maximum fund size of ESVCLPs will be increased to $270 million, from $200 million.

The increases will apply to new and existing funds and to new investments they make, including where funds make further investments in businesses already held. ESVCLPs must remain in compliance with their existing investment plans or seek approval for a replacement plan.

The eligible venture capital investor program will be closed to new applications from 7.30PM (AEST) 12 May 2026.

This measure is estimated to decrease receipts by $10 million and increase payments by $14.7 million over the five years from 2025-26.

International tax measures

Foreign resident CGT regime

The Government will provide a time‑limited, targeted concession in the foreign resident CGT regime for investment in the renewables sector as part of the implementation of the 2024-25 Budget measures to strengthen the foreign resident capital gains tax regime.

The transitional arrangement will apply to foreign investors disposing of certain renewable energy infrastructure assets from commencement, being the first day of the next quarter after the amending legislation receives assent, until 30 June 2030. This concession balances ongoing Government support for Australia’s practical action on climate change, with the need to ensure the tax treatment of these assets aligns with the treatment of other assets in the longer term.

The Government will also ensure the concept of “real property” in Australia is determined by Commonwealth legislation rather than state and territory laws, with effect from 12 December 2006, when the regime was introduced.

Global Anti‑Base Erosion Rules (Pillar Two)

The Government will amend Australia’s global and domestic minimum tax legislation, introduced in 2024, to implement the side‑by‑side package agreed by the OECD/G20 Inclusive Framework on Base Erosion and Profit Shifting (BEPS) on 5 January 2026.

Implementing the side‑by‑side package will ensure Australia’s global minimum tax rules are consistent with those of other implementing jurisdictions and will deliver on the Government’s commitment to support the OECD/G20 efforts to reform the international corporate tax system.

The side‑by‑side package will apply from 1 January 2026.

Indirect Tax Concession Scheme – diplomatic and consular concessions

The Government has extended access to refunds of indirect tax (including GST, fuel and alcohol taxes) under the Indirect Tax Concession Scheme (ITCS).

New access to refunds has been provided to the European Union, Italy and Chile relating to the construction and renovation of their current and future diplomatic missions and consular posts. Tuvalu will also have ITCS access extended to its High Commission, current and future consular posts and applicable accredited staff.

Other tax-related measures

PAYG instalments

The Government will provide $10.9 million to the Australian Taxation Office to expand its pilot of dynamic pay as you go (PAYG) instalment calculations, and will expand access to monthly payments.

From 1 July 2027, small and medium businesses will be able to opt in to reporting and paying PAYG instalments monthly and to using an ATO-approved calculation embedded in accounting software to calculate and vary their instalments. This will support businesses by enabling tax instalments to better reflect real time business activity. Taxpayers with a demonstrated history of non‑compliance will be required to report and pay PAYG instalments monthly.

Compliance activities

The Government will provide $86.3 million over four years from 1 July 2026 and $9.7 million per year ongoing from 2030-31 to deliver Phase 2 of the Counter Fraud Strategy to modernise the prevention and detection of fraud in the tax and super systems. This proposal will enhance the ATO’s ability to detect and prevent fraud in real time, provide additional fraud protections for individuals and expand live monitoring of fraudulent account access to tax agents, business and for high‑risk superannuation changes.

The Government will also strengthen the ATO’s ability to combat fraud by tax agents and other intermediaries. The ATO will be given powers to pause the recovery of tax debts of taxpayers who are victims of fraud by tax intermediaries, and waive those debts in appropriate circumstances, and to recover the debts from the tax intermediaries. Existing garnishee powers will also be expanded to include jointly held assets in circumstances where such arrangements are being used to frustrate recovery actions.

The Government will also progress further targeted exceptions to tax secrecy and enhancements to tax regulators’ information‑gathering powers to support integrity, compliance and effective administration of the tax system.

The ATO will undertake additional targeted compliance activities over the two years from 2026-27 to further address fraud in the system, including in relation to the Research and Development Tax Incentive.

Small business debts

The Government will provide $8.2m over three years from 2025-26 to extend the Small Business Debt Helpline financial counselling program and the NewAccess for Small Business Owners mental health coaching program to 30 June 2027.

Managed investment schemes

The Government will provide $17.8m over four years from 2026-27 (and $1.4m per year ongoing) to strengthen governance requirements, supervision and enforcement in relation to managed investment schemes, including:

- $10.3 million for ASIC to enhance its ability to utilise data in its supervision of the managed investment scheme sector;

- $7.6m over four years from 2026-27 (and $1.4m per year ongoing) for ASIC, the Office of the Australian Auditing and Assurance Standards Board and Treasury to strengthen governance requirements for managed investment schemes; and

- consulting publicly on new data collection powers in relation to managed investment schemes.

Large proprietary companies

The Government will relieve the reporting burden for large proprietary companies by increasing monetary thresholds from $50 million to $100 million of consolidated revenue and $25 million to $50 million of consolidated gross assets. Australian businesses that cease to meet these new thresholds would no longer need to lodge an annual audited financial report, directors' report or sustainability report.

Tariffs

The Government will abolish 497 more nuisance tariffs from 1 July 2026, resulting in the removal of almost 1,000 tariffs in two years. In addition, the Government will consult on abolishing another set of tariffs to cut costs for Australian businesses, strengthen competitiveness and enhance productivity.

Economic data

Here are some of the key numbers and forecast numbers revealed in the Budget.

Budget deficit: the deficit for 2025-26 is projected to be $28.3 billion (1% of GDP) for 2025-26, rising to $31.5 billion in 2026-27 and then falling to $25.3 billion in 2028-29.

Real GDP: 2.25% in 2025-26, falling to 1.75% in 2026-27 but rising to 2.25% in 2027-28.

Gross debt: $982 billion for 2025-26 (33.1% of GDP) and $1.050 trillion (34% of GDP) for 2026-27, rising to $1.120 trillion (35.2% of GDP) for 2027-28.

Net debt: $556 billion (18.8% of GDP) for 2025-26 and $616.6 billion (19.9% of GDP) for 2026-27, rising to $668.8 billion (21% of GDP) for 2027-28.

Unemployment rate: 4.25% for the June 2026 quarter, rising to 4.5% for the next three years.

Inflation: The impact of high global oil prices is expected to significantly add to inflationary pressures in the near term, with headline inflation forecast to be 5% through the year to the June quarter 2026, but declining to 2.5% through the year to the June quarter 2027(this is based on an assumed decline in global oil prices from the middle of 2026, a resolution of temporary pressures and a moderation in services inflation).

Wage price index: 3.25% in 2025-26 (ie through the year growth to the June quarter 2025), rising to 3.5% for 2026-27 and 2027-28.

Total tax receipts: $699.5 billion (23.6% of GDP) for 2025-26 and estimated to be $737.1 billion (23.8% of GDP) for 2026-27 and $757 billion (23.8% of GDP) for 2027-28.

Total payments: $788.1 billion (26.6% of GDP) for 2025-26 and estimated to be $829.6 billion (26.8% of GDP) for 2026-27, rising to $853.9 billion (26.8% of GDP) for 2026-27.

The Budget Papers point out that the global economic outlook remains uncertain and volatile. The conflict in the Middle East has created major disruptions in global oil supplies, with risks to domestic inflation and economic activity and the potential for large and negative flow-on implications for the revenue outlook. In other words, if the conflict in the Middle East is not resolved fairly quickly, the Treasury forecasts will almost certainly have to be revised.

DISCLAIMER

TaxWise® News is distributedby professional tax practitioners to provide information of general interest totheir clients. The content of this newsletter does not constitute specificadvice. Readers are encouraged to consult their tax adviser for advice onspecific matters.