From the ATO

Turning a hobby into income?

You might not think you’re running a business from your hobby or “side hustle” activities. If you’re starting to earn money from doing these activities regularly, you may be carrying on a business without realising it.

Generally, a business involves a set of continuous and repeated activities you do for the purpose of making a profit. Profit can be in money, but it can also be made through other means, like being paid with goods or services (such as a barter deal).

Activities that indicate you are operating a business can include:

- keeping records of your work;

- obtaining and maintaining any necessary licences or permits;

- regularly providing goods or services.

Your activities are not a business when they are:

- a one-off transaction (unless it is the first step in carrying on a business or intended to be repeated);

- done as an employee;

- a hobby or recreation from which you don't seek to profit;

- a simple investment, such as passively holding shares on which you receive dividends or a rental property you let through an agent.

Even if you’re not in business, you may still need to declare certain payments you receive as assessable income in your income tax return. For example:

- rent or income from providing services;

- the market value of goods or services you receive in a barter deal;

- dividends from shares you own;

- payments from a one-off transaction.

If you enter into a one-off transaction, such as one that involves the sale of small-scale land subdivisions, you need to consider whether your profit from the transaction is assessable as ordinary income or a capital gain. You may also be carrying on an enterprise in which case you may need to register for GST.

Tip!

Talk to your tax adviser if you are uncertain whether you are operating a business or need to register for GST.

Car expenses – logbook method

If you use the logbook method for claiming car expenses, including if you are an unincorporated sole trader, you need keep the following types of records:

- odometer records for the start and end of the period you own the car during the income year you rely on the logbook;

- proof of purchase price, or a new lease agreement and lease payment records;

- decline in value calculations;

- fuel and oil receipts, or records of a reasonable estimate of these expenses, based on odometer readings;

- if you have an electric or plug-in hybrid car, receipts from commercial charging stations or evidence showing you incurred additional electricity costs to charge the car at home, such as an electricity bill and the calculation of the direct cost to recharge – you cannot claim any commercial charging costs if you use the home charging rate of 4.2 cents per kilometre for a reasonable estimate of home charging, based on odometer readings. If the car is a plug-in hybrid, a specific formula must be used to calculate home charging expenses;

- registration and insurance – evidence of payment;

- servicing, repairs and tyres – evidence of payment.

Do you need a new logbook?

You can keep the same logbook for your car for 5 years, but there are circumstances where you may need a new one during that period. Relying on a logbook that no longer represents work-related travel may result in you claiming more, or less, than you are entitled to.

A new logbook may be required when you:

- change jobs;

- move to a new house or workplace; or

- have changes to your pattern of use of the car for work purposes.

If you use the logbook method for 2 or more cars, you need to keep a logbook for each car and make sure they cover the same period.

If you purchase a new car during the income year and want to continue relying on your previous car's logbook, you must make a nomination in writing. The nomination must be made before you lodge your tax return and state:

- you are replacing your original car with a new car; and

- the date that nomination takes effect.

Remember, if your employer provides you with a car or you salary sacrifice a car using a novated lease, you aren't entitled to claim work-related car expenses using the logbook or cents per kilometre method. This is because you don't own the car.

Compare your business with industry standards

Are you a sole trader? You can compare your business's performance against others in your industry by using the ATO’s small business benchmarks.

The ATO states that its benchmark methodology has been verified as statistically valid by an independent organisation and is consistent with international approaches. If you want to know more about the methodology, you can visit the ATO website - Benchmarking methodology

The benchmarks:

- are based on the biggest data set available;

- account for businesses with different turnover ranges across 100 industries;

- are published as a range to recognise the variations between businesses and different locations and circumstances.

The ATO allocates business data to a business type based on a combination of:

- business industry code;

- the main business activity listed on the tax return;

- the trading name label of the business.

The ATO has published on its website the latest performance benchmarks, based on information reported on tax returns for the 2023–24 income year, for approximately 100 industries. There is a good chance that the industry your business is part of is covered.

Tax Time 2026 – trusts

The ATO’s modernisation program is focused on trusts, and delivering three key objectives:

- streamlining the lodgment experience;

- improving the quality, accuracy and integrity of trust and beneficiary reporting; and

- better targeting of compliance and assurance activities.

The modernisation program is being delivered in a phased approach. Tax Time 2024 saw the introduction of the Trust income schedule to help all beneficiaries understand their income entitlements and new capital gains labels that support more accurate calculations for capital gains.

From 1 July 2026, the ATO will use trust statement of distribution data to pre-fill income tax returns for individual beneficiaries. This should make it easier for taxpayers to report their trust income accurately while improving the integrity of beneficiary reporting.

Tax Tips

How to reduce your tax bill

We are getting near the end of the tax year (30 June), so you might want to consider ways to reduce your tax bill.

The two simplest ways to do this are to reduce assessable income or increase deductible expenditure. Either way, your taxable income (and thus the amount of tax payable) is reduced.

One way to reduce assessable income for the current income year is to delay sending an invoice to a customer until after 30 June, if you report income on a cash basis. Of course, cash flow issues may dictate otherwise.

If you are in the process of selling property and the profit will be taxable as a capital gain, you could defer the sale until the next income year – but remember that the liability to pay capital gains tax (CGT) arises when you exchange contracts and not on settlement.

You can increase deductible expenditure by bringing it forward from the next income year to the current income year. This is particularly useful where an immediate deduction is available — for example, for depreciating assets costing less than $20,000 if you are a small business which uses the simplified depreciation rules, start-up costs and certain prepaid expenses.

Charitable donations are a good way to increase your deductions. If you are not sure if a donation will be deductible, you can check the deductibility status of charities at https://www.abn.business.gov.au/Tools/DgrListing. In certain circumstances, a deduction is available where trading stock is donated. Don’t forget to ask for a receipt.

What are the benefits?

If you are a sole trader or a partner in a partnership, the benefits of reducing your taxable income could include:

- reducing your marginal tax rate, for example, from 37% to 30%, or from 30% to 16%; and

- avoiding liability for the Medicare levy surcharge (MLS) (at least 1% of your income for MLS purposes) if you do not have appropriate level of private health insurance hospital cover.

In addition, the lowest marginal rate for individuals will decrease from 16% to 15% from 1 July this year, so there is a small benefit in taking steps that will reduce your taxable income this year even though it increases it next year.

Tip!

As the end of the income year approaches, talk to your tax adviser about ways to minimise your tax bill.

Pay less capital gains tax (CGT)

You can reduce the capital gains you've made by offsetting them with any capital losses, including from previous years. This will reduce your CGT bill. You need to use losses you’ve carried forward from previous years before using current year losses. If losses from previous years reduce your current year gains to zero, you can carry over any remaining losses to offset future gains for as long as you need.

You can choose which gains to offset. The only exception is gains you make from collectables, such as artwork, jewellery and antiques. You can only use a capital loss from collectables to offset a capital gain from collectables.

Think carefully about which gains you want to offset first. Starting with gains that aren’t eligible for the CGT discount will help reduce your CGT as much as possible.

You can’t offset a gain with a loss you've made from certain assets, including:

- personal use assets, such as boats or furniture;

- CGT exempt assets, such as cars and motorcycles;

- collectables that cost you $500 or less (if they cost more, the loss can only be offset against gains from collectables).

Tip!

Talk to your tax adviser if you have capital losses.

Superannuation Issues

Does your total super balance exceed $3 million?

From 1 July 2026, if your total super balance (TSB) at the end of the financial year exceeds the large super balance threshold (LSBT) (set at $3 million for the 2026–27 financial year) you will be subject to Division 296 tax of 15% on the proportion of earnings relating to your TSB that exceeds the LSBT.

Further, if your TSB at the end of the financial year exceeds the very large super balance threshold (VLSBT) (set at $10 million for the 2026–27 financial year) you will be subject to additional Division 296 tax of 10% on the proportion of earnings relating to your TSB that exceeds the VLSBT.

For subsequent years, in considering whether you have exceeded the LSBT or VLSBT for a financial year and are liable to Division 296 tax, your TSB used will be the greater of your TSB amounts either immediately before, or at the end of, that financial year.

These thresholds will be indexed incrementally to the consumer price index. The LSBT is indexed in $150,000 increments. The VLSBT is indexed in $500,000 increments.

Most funds will be required to calculate relevant super earnings for their members and then report those amounts to the ATO. Defined benefit funds will be required to report certain components for the ATO to calculate their member's relevant super earnings.

Total super balance

The new law also changes the definition of TSB.

From 1 July 2026, an individual’s TSB will be calculated as the sum of the TSB values for each of their Australian superannuation interests. The TSB value will be determined using a method or value prescribed in the regulations.

The TSB change ensures annual valuation requirements and removes the link to transfer balance account (TBA).

Superannuation interests in foreign funds are excluded from an individual's TSB.

Low Income Superannuation Tax Offset (LISTO)

Also, as part of the new law, from 1 July 2027 the LISTO income threshold will increase from $37,000 to $45,000 matching the top of the second income tax bracket. The maximum payment will also increase to $810.

Tip!

Talk to your professional adviser if you think the new rules may affect you.

Is your electronic service address (ESA) up to date?

If you have a self-managed super fund (SMSF) it needs to have an active ESA to comply with Payday Super and SuperStream changes.

If you receive super guarantee contributions from unrelated employers you must have an active electronic service address (ESA). An ESA is a digital address used to deliver SuperStream messages to your SMSF, typically through an administrator or messaging provider (see below).

This is even more important with Payday Super.

If your SMSF receives contributions from unrelated employers, you need to act now to ensure:

- your bank account is reachable via the New Payments Platform (NPP);

- you’re registered for, and continue to maintain, an active ESA.

Under new SuperStream upgrades to support Payday Super, there are new error messages and a new member verification request that employers will use to confirm the ESA is active before they can make a contribution, or continue to make contributions to the SMSF.

If your ESA is inactive or incorrect, the employer will receive an error message and will be prevented from making a contribution to the SMSF. This will delay any contribution, and may expose the employer to the super guarantee charge (SGC).

If the employer doesn’t have the correct details, they may open an account with a default super fund to avoid the SGC.

An active ESA is a critical requirement for SMSFs to comply with SuperStream obligations. Act now and review your details to confirm your ESA is active so your SMSF is prepared.

SMSF messaging providers

Your SMSF can only have one ESA address recorded with the ATO. This means if you require both contributions and rollovers or release authorities, then you need to select a provider that offers both services.

The ATO has a register of self-managed super fund (SMSF) messaging service providers who can provide an electronic service address (ESA) for contributions, rollovers and release authorities. These are listed below (note that the ATO does nor recommend or endorse any particular provider).

TBAR lodgment reminder for April 2026

All self-managed super funds (SMSFs) must report transfer balance account (TBA) events on a quarterly basis by lodging a transfer balance account report (TBAR). These events must be reported irrespective of the member's total superannuation balance.

TBARs for the March quarter are due on 28 April 2026.

If no TBA event has occurred during the quarter, then no lodgement is required.

You may need to lodge a TBAR sooner where your member has exceed their personal transfer balance cap.

Tip!

If you need help with your TBAR, talk to your professional adviser.

Before investing, understand your SMSF obligations

An SMSF exists for the sole purpose of providing retirement benefits to members. You must ensure your investments do not give you, your relatives or other related parties a present-day benefit.

Your SMSF must not do the following:

- lend money or provide financial assistance to members or their relatives;

- acquire assets from related parties, unless specific exceptions apply;

- exceed the in-house asset limits;

- enter into arrangements that do not follow arm's length rules.

Transactions with related parties must reflect market value. If an investment involves a related party or business activity, you should make sure you understand how the rules apply before proceeding.

If you fail to meet your obligations, you may face penalties, disqualification, or the fund losing its compliance status.

If you are considering an investment, take time to:

- review the investment restrictions that apply to SMSFs;

- consider whether the arrangement provides a current day benefit;

- ensure the structure and purpose of the investment are consistent with super law.

Understanding your obligations helps protect your retirement savings and supports the integrity of the super system.

Tip!

Talk to your professional advice if you are unsure if an investment you are contemplating might not be lawful.

General transfer balance cap indexation

Indexation of the general transfer balance cap will occur on 1 July 2026. The cap will increase by $100,000 from $2 million to $2.1 million. The defined benefit income cap (DBIC) will increase to $131,250 (from $125,000) for the 2026–27 income year.

This increase has flow through impacts for individuals with a personal TBC. These individuals will be entitled to an increase of their cap if they have not previously been at, or exceeded, their cap. Their increase will be a proportion of the $100,000 and will depend on their unused cap space. Individuals starting a pension for the first time on or after 1 July 2026 will be entitled to a personal TBC of $2.1 million.

The ATO will calculate an individual’s personal TBC based on the information reported to and processed by the ATO. To help individuals have a clear understanding of their position, the ATO encourages funds and advisers to report all TBC events when they occur and as early as possible before the 1 July 2026 indexation start date.

Indexation of the general TBC has flow through consequences for the Total Super Balance (TSB) thresholds. The TSB influences an individual’s non-concessional contributions cap, non-concessional bring forward arrangement, carry-forward concessional contributions, the work-test exemption and eligibility for the spouse tax offset and co-contributions.

Setting up an SMSF - choose the trustee structure

You can choose one of the following trustee structures for your self-managed super fund (SMSF):

- individual trustees;

- a corporate trustee (a company acting as trustee for the fund).

Member and trustee requirements

If you choose individual trustees:

- your SMSF can have up to 6 members;

- each member of the SMSF must be a trustee;

- each trustee must be a member of the SMSF (single-member funds must have 2 trustees, only one must be a member);

- members cannot be an employee of another member unless they are relatives.

Some State and Territory laws restrict the number of trustees a trust can have to less than 6.

If you choose a corporate trustee:

- each member of your SMSF must be a director of the corporate trustee;

- for a single-member fund, the member can be either the sole director of the corporate trustee or one of 2 directors of the corporate trustee provided either the member and other director are relatives or the member is not an employee of the other director;

- directors of corporate trustees must have a director identification number – see below.

Governing rules

Individual trustees and directors of the corporate trustee must follow the rules in the:

- SMSF trust deed; and

- tax and super laws.

In addition, directors of the corporate trustee must follow the rules in the:

- company's constitution; and

- Corporations Act 2001.

Directors of a corporate trustee must obtain a director identification number (director ID), which is a unique identifier that a director will apply for once and keep forever. Funds identified with a corporate trustee structure that don't have a director ID will be unable to proceed. Penalties may be imposed by ASIC if directors don't have a director ID.

Ownership of SMSF assets

All fund assets must be:

- kept separate from the personal assets of trustees and directors;

- in the name of the fund or the name of the individual trustees 'as trustees for' the fund.

If your SMSF has individual trustees, when a trustee is added or removed, the name in each asset's ownership document must be updated. This can be costly and time-consuming. State government authorities and financial institutions may charge a fee for title changes.

If your SMSF has a corporate trustee, when a person starts or stops being a member, they become, or cease to be, a director of the corporate trustee.

The name on the ownership documents doesn't change. It remains in the name of the corporate trustee.

Succession

SMSFs with individual trustees must always have at least 2 trustees. If your fund has 2 individual trustees and one trustee leaves or dies, you must do one of the following:

- appoint another trustee;

- change to a corporate trustee structure; or

- wind up the fund.

If you appoint another individual trustee, you need to notify the ATO within 28 days.

Funds with a corporate trustee can operate with one director. The corporate trustee does not change if a director leaves or dies. However, if the directors change, you need to notify the ATO and ASIC within 28 days.

Tip!

If you are thinking of setting up an SMSF or changing the structure of your SMSF, talk to your professional advisers.

Claiming SMSF setup costs correctly

If you paid your SMSF (self-managed super fund) setup costs personally, you may be able to claim reimbursement from the fund.

To do this correctly:

- the SMSF must charge the costs against your benefits;

- you should seek reimbursement as soon as the fund has enough cash;

- the reimbursement must relate to costs incurred in setting up the fund – not for other services.

When done properly, reimbursement isn’t considered a contribution, borrowing or financial assistance. But if you don’t seek reimbursement for set up costs charged to your fund, the ATO will treat your payment as a contribution.

Keep in mind that SMSF establishment costs are capital expenses and can’t be claimed as a deduction. You can’t be paid for any trustee duties, even if you set the fund up yourself. If your fund uses a corporate trustee, ASIC registration and annual fees will apply.

Education direction

If you breach your obligations under the law when operating your SMSF (which you could do inadvertently), the ATO may ask you to complete an SMSF education course.

An education direction is a formal notice requiring a trustee (or director of a corporate trustee) to complete an approved SMSF education course within a set time. This helps ensure they understand their legal obligations and responsibilities going forward.

When someone receives an education direction, they must:

- complete the course by the due date, and

- sign a new trustee declaration (NAT 71089) within 21 days.

Accessing your super early may be illegal

Your SMSF must operate solely to provide retirement benefits. Arrangements that divert funds for other purposes put those benefits, and your fund’s compliance, at risk.

If someone offers to help you access your super early, or advises you that you can use a self-managed super fund to pay off business debts, buy a car or pay for a holiday, this is not true and is illegal.

Promoters often present SMSF schemes as legitimate investment opportunities. They may promise high returns, tax advantages, or early access to super. Some arrangements use complex structures to make the offer look compliant − even when they breach the law. Promoters may also advertise their arrangement as ATO-approved. The ATO does not approve specific investment products or schemes.

Be cautious if an offer:

- sounds unusually profitable or low risk;

- promises access to super before you meet a condition of release

- involves complex or artificial structures you don't understand;

- pressures you to act quickly;

- requires you to move super into a newly established SMSF for a specific investment.

There are serious consequences if you access super illegally. You may be disqualified from being an SMSF trustee, which goes on the public record. Additional tax, penalties and interest may also apply.

You can report any person recommending an illegal access to super scheme using the ATO’s tip off form.

Tip!

Talk to your professional adviser before accessing your super.

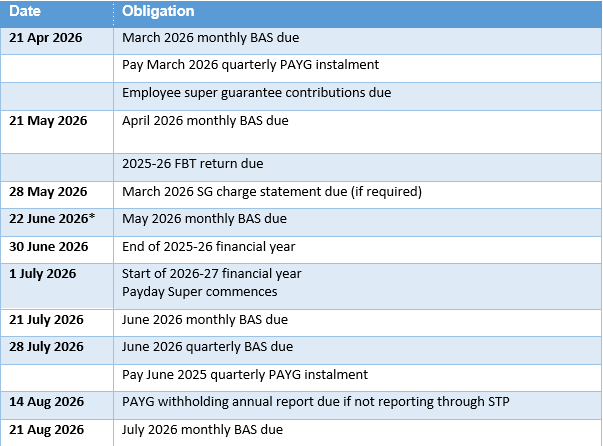

Key tax dates

Note!

Talk to your tax agent to confirm the correct due dates for your own tax obligations. For example, you may have more time to lodge and pay if impacted by a natural disaster.

DISCLAIMER

TaxWise® News is distributed by professional tax practitioners to provide information of general interest to their clients. The content of this newsletter does not constitute specific advice. Readers are encouraged to consult their tax adviser for advice on specific matters.